You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Guaranteed issue rights – also known as “Medigap protections” – require insurance carriers to let you enroll in a Medigap policy, prohibiting them from denying you coverage or charging you more for coverage based on your medical history.1

Medigap differs from Original Medicare, Medicare Advantage, and Medicare Part D, because there’s no annual open enrollment period for Medigap in most states.2

Medicare beneficiaries have a six-month initial enrollment period for Medigap. It begins when:

During that initial enrollment period, any Medigap plan in your area must allow you to enroll regardless of your medical history.

After that window ends, certain life events will trigger guaranteed issue rights for Medigap plans, creating a special enrollment period during which you can enroll in a new Medigap plan regardless of your medical history.

Some states offer annual opportunities to enroll in Medigap or switch to a different Medigap plan, and a few states offer year-round guaranteed-issue access to Medigap plans. But in most states, Medigap insurers consider an applicant’s medical history if the person applies without a guaranteed issue right and after their initial enrollment period has ended.

This means the insurer can consider the person’s medical history when determining whether to offer coverage and if so, what the premium will be. This can make it difficult or impossible for some applicants to enroll in new Medigap coverage if they have pre-existing medical conditions.3

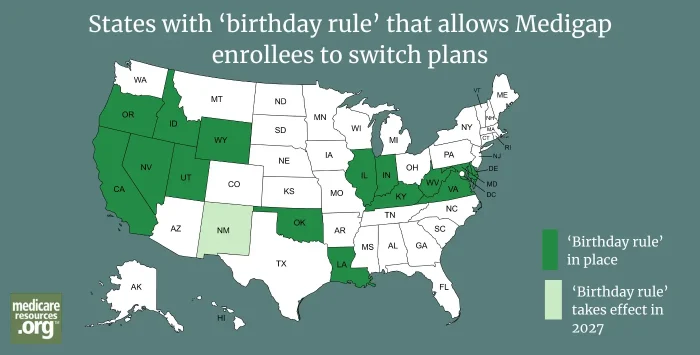

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

Footnotes