You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Medicare Advantage (Medicare Part C) is a coverage alternative to Original Medicare. Medicare Part C plans are offered by private insurers approved by Medicare. In 1997, Congress passed legislation creating the Medicare+Choice program, which was renamed Medicare Advantage under the Medicare Prescription Drug, Improvement, and Modernization Act of 2003.1

As of June 2024, there were nearly 34.1 million people covered by Medicare Advantage, accounting for just over half of the more than 67.5 million total Medicare beneficiaries. (The rest had Original Medicare.)2 Enrollment in these plans has grown significantly over the years. In 2007, only 19% of Medicare beneficiaries had Medicare Advantage plans.3

All Medicare Advantage plans are required to cover services that are covered by Medicare Part A and Medicare Part B (except hospice services, which are covered under Original Medicare for all beneficiaries).4 However, the out-of-pocket costs for these services vary widely between Original Medicare and Medicare Advantage. And there can be different coverage rules under Medicare Advantage plans, such as a requirement to use in-network medical providers or obtain prior authorization.

This differs from one Medicare Advantage plan to another, and also differs from Original Medicare. Original Medicare allows beneficiaries to use any provider who accepts Medicare, and prior authorization is very rarely used in Original Medicare.

Medicare Advantage enrollees only have one plan, rather than having to use multiple plans to get coverage for all the care they need. (Original Medicare does not have a cap on out-of-pocket costs and does not cover outpatient prescription drugs, so most Original Medicare enrollees rely on additional coverage, including Medigap plans and stand-alone Medicare Part D plans.)5

Since 2019, Medicare Advantage plans have been allowed to cover a broader range of extra benefits than they could in prior years4 and some Medicare Advantage plans have chosen to offer these benefits. As of 2025, 99% of Medicare Advantage plans offer some type of extra benefit not covered by Original Medicare6 (in some plans, different benefits are available to different enrollees depending on availability and health status.7

Medicare Open Enrollment – also known as the Annual Election Period – runs from October 15 to December 7 each year. This is an opportunity for Medicare beneficiaries to switch to a different Medicare Advantage plan or enroll in one for the first time. Plan selections made during this window will take effect January 1 of the following year.

Read our Guide to Medicare Open Enrollment.

In addition, a Medicare Advantage Open Enrollment Period – from January 1 through March 31 – is an opportunity for people already enrolled in Medicare Advantage to switch to another Medicare Advantage plan or to switch to Original Medicare.8

Read our overview of the Medicare Advantage Open Enrollment Period.

The cost of a Medicare Advantage plan varies depending on the plan you select. Medicare Advantage enrollees pay the Medicare Part B premium ($185/month for most beneficiaries in 2025),9 although some Medicare Advantage plans cover a portion of this cost for their enrollees.

Across all Medicare Advantage plans with integrated Part D coverage (MA-PDs), the average premium (in addition to the Medicare Part B premium) is $13.32/month in 2025, and it’s projected to decrease to $11.50/month in 2026.10 But more than three-quarters of MA-PD enrollees pay no premium in 2025, other than the premium for Part B. In other words, they’re in “zero premium” plans.6 These plans don’t charge a monthly premium and enrollees only have to pay the premium for Medicare Part B.

Average MA-PD premiums tend to be lower for HMOs versus PPOs. In 2025, KFF reported that the average HMO MA-PD had a premium of $11/month, whereas the average local PPO had a premium of $15/month and the average regional PPO (which represents a very small share of enrollment) had a premium of $75/month.6

The majority (54%) of 2025 Medicare Advantage enrollees are in HMOs. Local PPOs account for 45% of enrollees in 2025. Regional PPOs are rare, accounting for just 1% of enrollees in 2025.6

If you already have Medicare Part A and Medicare Part B (or are eligible to enroll in them), you can choose to enroll in any Medicare Advantage plan available in your area, instead of Original Medicare. You can do this when you’re first eligible for Medicare, or during Medicare Open Enrollment (the Annual Election Period).

But there are some rural areas of the country where no Medicare Advantage plans are available for purchase.11 If you’re in one of those areas, Original Medicare is your only Medicare coverage option.

An increasing number of employers are using Medicare Advantage plans to provide health coverage to their retirees: About 17% of Medicare Advantage enrollees are enrolled in employer-sponsored Medicare Advantage plans.12

If you have employer-sponsored or union-sponsored health benefits, you may be able to add a Medicare Advantage plan, but you’ll want to discuss this with your benefits administrator first, to ensure that you won’t lose your existing health benefits if you enroll in a Medicare Advantage plan.

Special Needs Plans (SNPs) are Medicare Advantage plans that are specifically designed to cater to the needs of certain populations, such as individuals with certain chronic medical conditions. Institutional Special Needs Plans (I-SNPs) are for, among other things, people who live in long-term care skilled nursing facilities. In order to join any SNP, you would have to meet the specific eligibility requirements of the plan.13

There are five different types of Medicare Advantage plans14 although not all of them are available in all areas:

A few points to know about the different coverage types:

Yes, zero-premium Medicare Advantage plans are possible. But most enrollees do still have to pay the premium for Medicare Part B. (In 2025, the standard premium for Medicare Part B is $185/month.)9

As of 2025, 76% of all MA-PD enrollees only had to pay the Medicare Part B premium, as their plans did not have any additional premiums.6

Some Medicare Advantage plans pay some or all of the Part B premium on behalf of their enrollees, further reducing the monthly cost of the coverage.

People who are eligible for full Medicaid coverage (in addition to Medicare) do not have to pay Part B premiums19 And people who are eligible for a Medicare Savings Program may find that one of the programs covers the cost of Part B for them.20

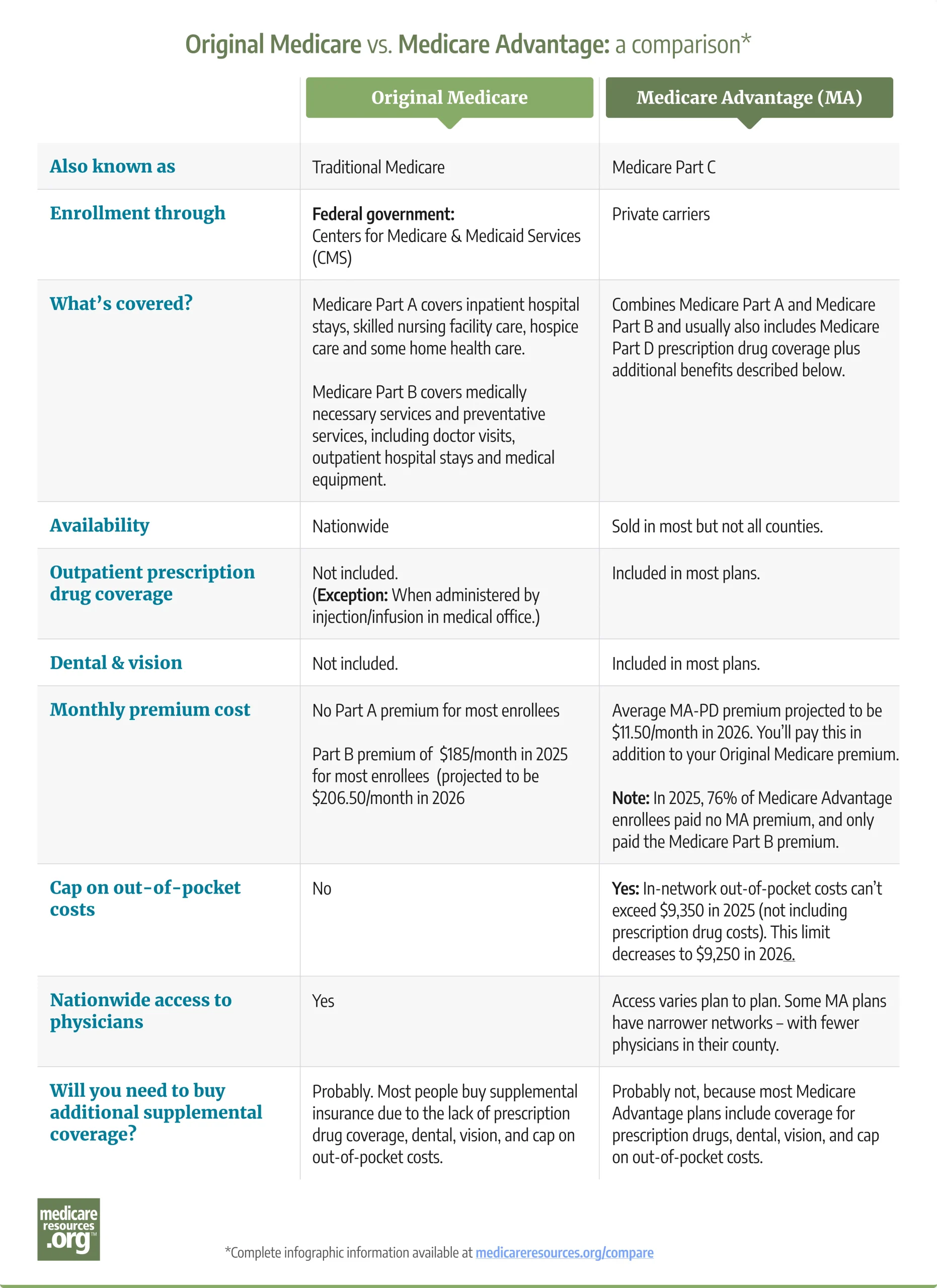

See transcription of this image.

Original Medicare vs. Medicare Advantage:

|

||

|---|---|---|

| Original Medicare | Medicare Advantage (MA) | |

| Also known as | Traditional Medicare | Medicare Part C |

| Enrollment through | Federal government:

Centers for Medicare & Medicaid Services |

Private carriers |

| What’s covered? | Medicare Part A covers inpatient hospital stays, skilled nursing facility care, hospice care and some home health care. Medicare Part B covers medically necessary services and preventative services, including doctor visits, outpatient hospital stays and medical equipment. |

Combines Medicare Part A and Medicare Part B and usually also includes Medicare Part D prescription drug coverage plus additional benefits described below. |

| Availability | Nationwide | Sold in most but not all counties.21 |

| Outpatient prescription drug coverage | Not included. (Exception: When administered by injection/infusion in medical office.) |

Included in most plans. |

| Dental & vision | Not included. | Included in most plans. |

| Monthly premium cost | No Part A premium for most enrollees.

Part B premium of $185/month in 2025 for most enrollees (projected to be $206.50/month in 2026)22 |

Average MA-PD premium projected to be $11.50/month in 2026. You’ll pay this in addition to your Original Medicare premium.

Note: In 2025, 76% of Medicare Advantage enrollees paid no MA premium, and only paid the Medicare Part B premium. |

| Cap on out-of-pocket costs | No | Yes: In-network out-of-pocket costs can’t exceed $9,350 in 2025 (not including prescription drug costs). This limit decreases to $9,250 in 2026.23 |

| Nationwide access to physicians | Yes | Access varies plan to plan. Some MA plans have narrower networks – with fewer physicians in their county. |

| Will you need to buy additional supplemental coverage? | Probably. Most people buy supplemental insurance due to the lack of prescription drug coverage, dental, vision, and cap on out-of-pocket costs.. | Probably not, because most Medicare Advantage plans include coverage for prescription drugs, dental, vision, and cap on out-of-pocket costs. |

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written hundreds of opinions and educational pieces about the Affordable Care Act and Medicare for healthinsurance.org and medicareresources.org.

During the Medicare Advantage open enrollment period (MAOEP) – from Jan. 1 to March 31 – Medicare Advantage enrollees may be able switch their plan – or drop it. Learn about restrictions and how to make changes.

An overview of 2025 premiums and out-of-pocket costs for Original Medicare, Medicare Advantage, Medigap and Medicare Part D.

Beyond your initial opportunity to enroll in Medicare plans, the federal government provides other windows for enrollment and plan changes each year.

Thousands of Medicare beneficiaries change their coverage each year during several enrollment windows. Find out how and when you can switch plans.

During the Medicare Advantage open enrollment period (MAOEP) – from Jan. 1 to March 31 – Medicare Advantage enrollees may be able switch their plan – or drop it. Learn about restrictions and how to make changes.

An overview of 2025 premiums and out-of-pocket costs for Original Medicare, Medicare Advantage, Medigap and Medicare Part D.

Beyond your initial opportunity to enroll in Medicare plans, the federal government provides other windows for enrollment and plan changes each year.

Thousands of Medicare beneficiaries change their coverage each year during several enrollment windows. Find out how and when you can switch plans.

Footnotes