You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Like other types of health insurance, each of the various types of Medicare has a special enrollment period (SEP) that’s triggered by various qualifying life events. SEPs allow a person to sign up for coverage outside of the usual initial enrollment or annual open enrollment windows.

But the Medicare SEP rules vary depending on the type of coverage. So if you’ve moved, or retired and strategically delayed your enrollment, a Medicare SEP might be helpful, giving you flexibility when events in your life affect your coverage needs.

The eligibility rules for a Medicare SEP differ for each type of coverage, but the life events that make a beneficiary eligible may include (depending on the type of coverage): a change in residence, a change in eligibility for Extra Help, loss of coverage due to a change in employment, or Medicare plan contract changes. Life events that may trigger an SEP for each type of coverage are listed in the sections below.

If you’re aging into Medicare, you can enroll during your seven-month initial enrollment period that begins three months before the month you turn 65.1 If you miss that window, you have an annual opportunity to sign up for coverage during the January – March general enrollment period2. (A late-enrollment penalty will apply if you’ve delayed your enrollment by 12 months or more from when you were initially eligible.)

But if you qualify for a special enrollment period, you don’t have to wait for the general enrollment period to sign up for coverage, and you may also be able to avoid late-enrollment penalties. Some eligibility requirements for a special enrollment period have been available for many years, while others became available as of 2023 under rules that were finalized in 2022.3

This special enrollment period allows a person to sign up for Medicare Part B, Premium Part A, or both. Most people do not have to pay a premium for Medicare Part A, and can enroll in that coverage any time after they become eligible.4 A special enrollment period is only necessary for Medicare Part A if you have to pay a premium for it. It’s called “Premium Part A” if you have to pay a premium for the coverage, but 99% of Medicare beneficiaries do not have to pay a premium for Part A.5

Here’s a list of life events that may make you eligible for a special enrollment period:6

Any special enrollment right to sign up for Medicare Part B (and Premium Part A) will allow you to choose either Original Medicare or Medicare Advantage.

A special enrollment period for Medicare Part A is only necessary if you’d have to pay a premium to enroll in Part A. About 99% of Medicare beneficiaries do not have to pay a premium for Part A.5 For these individuals, enrollment in Part A is available starting when they’re first eligible or any time after that.4 Your coverage effective date may be backdated by up to six months (but no earlier than the month you were first eligible).

If you’re enrolled in a Medicare Advantage or Medicare Part D prescription drug plan, you can make changes to your coverage during Medicare open enrollment each fall.

But there are a variety of qualifying life events that allow you to switch to a different plan outside of the annual election period.10 (Depending on the circumstances, there may also be an option to switch to Original Medicare.) Here are situations considered qualifying life events that may trigger a SEP:

Medigap (Medicare supplement insurance) is unique among the various types of Medicare coverage, in that it does not have a federally mandated annual enrollment period.13

Some states do have limited annual enrollment opportunities, but federal rules only require all Medigap plans to be guaranteed issue (meaning eligibility and premium do not depend on medical history) during a six-month window that starts with your Part B effective date, assuming you’re at least 65 years old. (You must also have Medicare Part A to buy a Medigap plan.)

After that, Medigap insurers in most states can use medical underwriting when a person applies for Medigap coverage. That means the insurer can reject the application or offer a policy with a higher premium, depending on the person’s medical history.

But there are certain situations where an insurance company can’t deny you a Medigap policy (or charge higher premiums based on medical underwriting), which are referred to as guaranteed-issue rights. (Unlike other types of Medicare coverage, a beneficiary can apply for a Medigap plan at any time, but the insurer can use medical underwriting if the person doesn’t have a guaranteed-issue right.)

In general, the guaranteed-issue special enrollment period continues for 63 days after the qualifying event, and in some cases it’s also available starting 60 days before the qualifying event. In most cases, a guaranteed-issue right will only allow you to enroll in Medigap Plan A, B, C, D, F, G, K, or L, as opposed to any available Medigap plan. (Note that regardless of the circumstances, Plans C and F can only be purchased by people who became eligible for Medicare prior to 2020. If you became eligible for Medicare in 2020 or later, you will have access to Plans D or G instead of Plans F or C.)14

There are a variety of qualifying events that result in a federal Medigap guaranteed-issue right. They include:

As noted above, some of these qualifying events will also trigger a special enrollment period to sign up for a Medicare Advantage plan. You’ll want to consider the pros and cons of Medigap plus Part D versus Medicare Advantage before making your decision.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written hundreds of opinions and educational pieces about the Affordable Care Act and Medicare for healthinsurance.org and medicareresources.org.

Eligibility for Medicare coverage depends on factors that include your work history, health status, and residency status. Check your eligibility today.

You may be eligible to enroll in Medicare Part A at age 65, but some seniors decide to delay their enrollment. Here's why.

If you were penalized for delayed Medicare Part B enrollment, you may have the penalty waived if you were advised to delay Part B, and now find you were given bad advice. Asking for the correction is known as requesting equitable relief.

Learn how and when to enroll in Original Medicare, Medicare Advantage, Medigap, and Part D coverage. Get plan information and a free quote today.

The Medicare Part B SEP allows people to delay Part B enrollment if they have health coverage through their own employer or a spouse’s current employer.

People who delay enrollment in Medicare Part B when they're first eligible may face a late-enrollment penalty for each year they delay signing up.

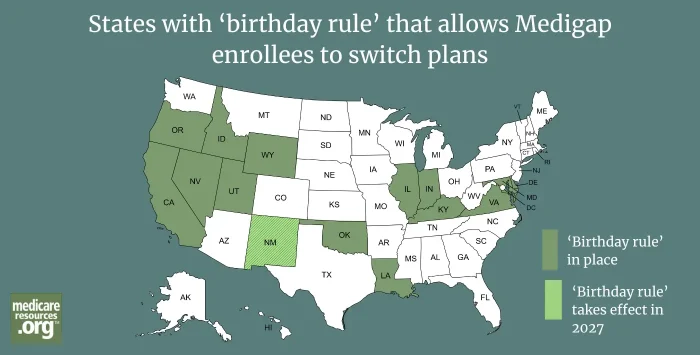

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

Eligibility for Medicare coverage depends on factors that include your work history, health status, and residency status. Check your eligibility today.

You may be eligible to enroll in Medicare Part A at age 65, but some seniors decide to delay their enrollment. Here's why.

If you were penalized for delayed Medicare Part B enrollment, you may have the penalty waived if you were advised to delay Part B, and now find you were given bad advice. Asking for the correction is known as requesting equitable relief.

Learn how and when to enroll in Original Medicare, Medicare Advantage, Medigap, and Part D coverage. Get plan information and a free quote today.

The Medicare Part B SEP allows people to delay Part B enrollment if they have health coverage through their own employer or a spouse’s current employer.

People who delay enrollment in Medicare Part B when they're first eligible may face a late-enrollment penalty for each year they delay signing up.

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

Footnotes