You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Medicare enrollees have an annual opportunity to review and adjust their Medicare coverage each year, but that flexibility doesn’t apply to Medicare Supplement insurance – commonly referred to as Medigap. While Medicare Advantage and Medicare Part D have an annual open enrollment period (October 15 – December 7), federal rules only give Medicare beneficiaries one guaranteed-issue Medigap open enrollment period in their lifetime.

Medigap plans help to pay out-of-pocket costs (deductibles, copays, and coinsurance) for services covered by Original Medicare. Depending on your medical situation, you could need more or less coverage at different times in your life. Unfortunately, having only one Medigap open enrollment period does not give enrollees the flexibility to change plans if they have (or later develop) pre-existing medical conditions.

The truth is that you may or may not be able to change Medigap plans when you need to. That’s because, although you can apply for a Medigap policy anytime, insurance companies in most states can use medical underwriting when you apply for a Medigap plan outside of the Medicare open enrollment period.

Under federal rules, Medigap open enrollment starts when you’re at least 65 and have enrolled in Medicare Part B (you also need Medicare Part A in order to get Medigap, but some people delay their Part B enrollment, which is why the Medigap enrollment window begins when Part B coverage begins). This initial enrollment window lasts for six months.1

(There is no federally required Medigap enrollment window for people under the age of 65 who qualify for Medicare due to a disability. But many states ensure that Medicare beneficiaries under 65 can sign up for Medigap plans. In that case, the beneficiary will also have another guaranteed-issue open enrollment window for Medigap when they turn 65, under federal rules.)1

The initial enrollment period allows Medicare beneficiaries to sign up for a Medicare supplement plan without medical underwriting. Put simply, it is a time when insurance companies cannot charge you higher rates or reject your application based on your medical history. After that enrollment period ends, insurers in most states can use medical underwriting if you apply for a Medigap plan, unless you qualify for a special enrollment period with guaranteed-issue rights.

(This is based on certain qualifying life events, but the list is more limited than the qualifying life events that apply to other types of coverage. For example, if you already have a Medigap plan and you move to a new state, it will not trigger a Medigap special enrollment period unless you’re enrolled in a specific type of Medigap coverage called Medicare SELECT. That’s because you can keep your Medigap plan (unless it’s Medicare SELECT) when you move to the new state, so there’s not a special enrollment period to switch to a different Medigap plan.)

To clarify, you can apply for a Medigap policy at any time as long as you have Medicare Part A and Part B. If you’re subject to underwriting — which will generally be the case in most states if you’re past your initial enrollment period and don’t qualify for a special enrollment period — the insurer will determine whether to offer you coverage, and at what price, based on your medical history. So some people will have no trouble switching Medigap plans, while others will find it expensive or impossible.

Fortunately, there are Medigap protections in place that may qualify you for a special enrollment period. Your birthday may be one of them, depending on where you live.

You may qualify for a special Medigap enrollment period if you have guaranteed issue rights. In these cases, insurance companies cannot charge you more based on your medical conditions, put a waiting period on your coverage, and deny you coverage.

The Centers for Medicare and Medicaid have established a list of seven situations that require insurance companies to allow you to sign up for or change a Medigap plan without medical underwriting. This list of events is somewhat limited, but you may have even more options depending on what state you live in.

As of 2026, roughly half the states offer Medigap guaranteed issue rights that go above and beyond what the federal government requires (this applies to annual enrollment or plan change opportunities; more than half the states go above and beyond federal requirements in terms of making guaranteed-issue Medigap plans available to beneficiaries under age 65).

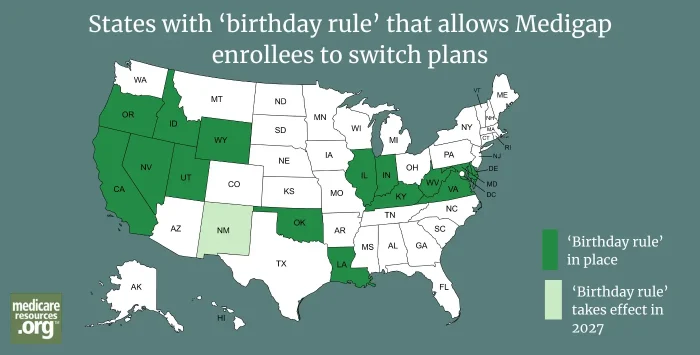

Of the states where Medigap enrollment and plan change opportunities go beyond federal requirements, 16 have implemented a “birthday rule” that allows Medigap enrollees to switch Medigap plans without medical underwriting around the time of their birthday. (Several additional states have other windows, either year-round, or a specific time of the year, or related to the anniversary of when the person’s current policy was purchased.)

To qualify for a “birthday rule” plan change, you must already be enrolled in a Medigap plan. In most cases, a birthday rule enrollment window will allow you to switch (without underwriting) to any available Medigap plan that has the same or lesser benefits as the plan you already have.

But in Indiana and Virginia, the birthday rule only allows you to switch (without underwriting) to a policy that offers the same benefits as your current policy (so if you have Medigap plan G, you can only switch to another Plan G, for example).

And in Kentucky, Louisiana, Utah, and West Virginia, the birthday rule only allows you to switch to a policy with equal or lesser benefits that’s offered by your current insurer (or in some cases, an affiliated insurer), rather than a policy offered by any insurer in your area.

Here are details for each state’s birthday rule:

If you live in one of these states, you may want to consider taking advantage of these birthday rules as long as you understand how they work.

While Medigap is an excellent option for people on Original Medicare, some policyholders may feel that they are locked into Medigap plans with high rates. Guaranteed issue rights can help, but the situations outlined by CMS are limited to very specific situations that apply to relatively few policyholders.

The states that have created annual windows during which enrollees have at least some level of guaranteed-issue Medigap rights are helping to give Medicare beneficiaries the option to periodically review their Medigap options, even if they have pre-existing medical conditions.

The number of states offering “birthday rule” plan change windows has increased in recent years. Kentucky, Utah, Virginia, Indiana, Wyoming, Delaware, and West Virginia are the latest states to join this list, with plan change opportunities available starting in 2024, 2025, and 2026. New Mexico will join them in 2027.

But although birthday rules have been gaining traction with state lawmakers, they can also have downsides. Requiring insurers to accept enrollees regardless of their medical history can result in higher premiums for all enrollees, and fewer insurers choosing to offer Medigap plans in the state.13,14 This is something that lawmakers and state insurance departments must take into consideration when deciding what sorts of guaranteed-issue consumer protections to put in place for Medigap plans.

Additional states are considering Medigap “birthday rule” legislation in 2026, including:

Several states considered legislation in recent years to create birthday rules, but the bills did not pass:

Lawmakers in those states may try again in a future year, and other states might consider this as well. Keep an eye out for more “birthday rules” in the future.

Tanya Feke, M.D. is a licensed, board-certified family physician living in New Hampshire. As a practicing primary care physician in Connecticut and an urgent care physician in New Hampshire, she saw first-hand how Medicare impacted her patients. In recent years, her career path has shifted to consultant work with a focus on utilization management and medical necessity compliance.

Dr. Feke is an expert in the field, having Medicare experience on the frontlines with patients, hospital systems, and insurers. To educate the public about ongoing issues with the program, she authored “Medicare Essentials: A Physician Insider Reveals the Fine Print.” Her analysis of Medicare issues is frequently referenced by the media, and she is a contributor to multiple online publications.

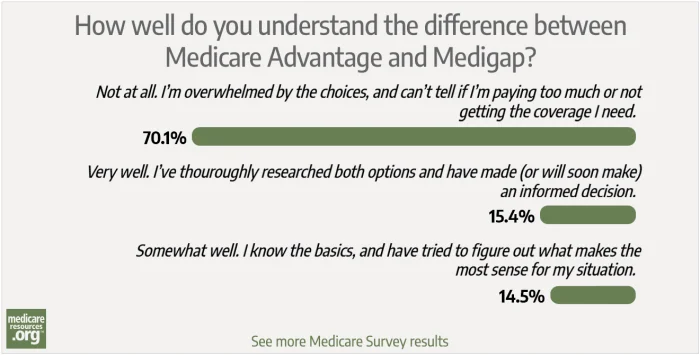

More than two-thirds of the respondents in our most recent survey indicated that they don’t understand the differences between Medicare Advantage and Medigap and are overwhelmed by the available choices.

The best time to enroll in a Medicare supplement plan is during your Medigap open enrollment period, a six-month window that begins on the first of the month you're enrolled in Medicare Part B and are 65 or older.

Considering a change to your Medicare coverage? Consider these 10 factors when choosing between Medicare Advantage, Medigap, and Part D coverage.

Medicare supplement insurance, or Medigap, is insurance that supplements Original Medicare, covering some or all of the out-of-pocket costs that a beneficiary would otherwise have to pay for services covered by Original Medicare.

Modern Medigap plans do not include prescription drug benefits. Instead, Medicare offers prescription drug coverage under Part D. Medicare enrollees can get prescription coverage either by switching to a Medicare Advantage plan or by purchasing a stand-alone Medicare Part D plan (PDP) to go along with Original Medicare.

If you're like most Medicare enrollees, you probably aren't planning to make any changes to your existing coverage for the coming year, but – like most beneficiaries – you should probably at least consider it during Medicare's open enrollment period. And if you have Medicare Advantage, you also have an opportunity to change your coverage between January and March each year.

More than two-thirds of the respondents in our most recent survey indicated that they don’t understand the differences between Medicare Advantage and Medigap and are overwhelmed by the available choices.

The best time to enroll in a Medicare supplement plan is during your Medigap open enrollment period, a six-month window that begins on the first of the month you're enrolled in Medicare Part B and are 65 or older.

Considering a change to your Medicare coverage? Consider these 10 factors when choosing between Medicare Advantage, Medigap, and Part D coverage.

Medicare supplement insurance, or Medigap, is insurance that supplements Original Medicare, covering some or all of the out-of-pocket costs that a beneficiary would otherwise have to pay for services covered by Original Medicare.

Modern Medigap plans do not include prescription drug benefits. Instead, Medicare offers prescription drug coverage under Part D. Medicare enrollees can get prescription coverage either by switching to a Medicare Advantage plan or by purchasing a stand-alone Medicare Part D plan (PDP) to go along with Original Medicare.

If you're like most Medicare enrollees, you probably aren't planning to make any changes to your existing coverage for the coming year, but – like most beneficiaries – you should probably at least consider it during Medicare's open enrollment period. And if you have Medicare Advantage, you also have an opportunity to change your coverage between January and March each year.

Footnotes