You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Coinsurance refers to a percentage of medical costs that a person pays after meeting their health plan’s deductible. The patient will pay the full plan-approved amount until the deductible is met, and then a percentage of the cost of additional services during the coinsurance phase.

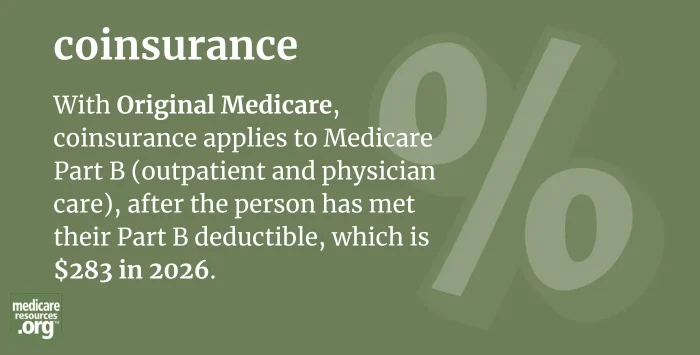

With Original Medicare, coinsurance applies to Medicare Part B (outpatient and physician care), after the person has met their Part B deductible, which is $283 in 2026.1 For most services covered by Medicare Part B, the coinsurance is 20% of the Medicare-approved amount, meaning the patient pays 20% and Medicare pays 80%.1

Under Medicare Part A, which covers inpatient care, there’s a deductible and then per-day copays after a certain number of days in the hospital or a skilled nursing facility. But Part A does not use percentage-based coinsurance.

Learn more about Medicare out-of-pocket costs, including the Part B coinsurance.

If you have a Medigap plan, it will pay some or all of the coinsurance that you’d otherwise have to pay for Medicare Part B, and it will also cover various out-of-pocket costs under Medicare Part A. Medigap plans will not cover any of your out-of-pocket costs for outpatient medications unless you still have Plan H, I, or J that you purchased before 2006. Medigap plans are standardized, and each plan differs in terms of what coinsurance costs it will pay. So the specifics of how your plan covers Medicare coinsurance will depend on the plan that you select.

Under Medicare Part D, coinsurance depends on your policy’s plan design. But a standard plan has a deductible (no more than $615 in 2025), and then the enrollee pays 25% coinsurance until their total out-of-pocket costs for covered drugs reach $2,100. At that point, the Part D plan starts to pay the full cost of their covered drugs for the remainder of the year.2 Plans can have other designs, however, including a lower (or no) deductible, or copays instead of coinsurance.

If you enroll in Medicare Advantage, your plan will wrap inpatient, outpatient, and in most cases, prescription coverage, into one plan. There will generally be copays for some services, while other services will have a deductible and then coinsurance that you’ll have to pay until you reach the plan’s out-of-pocket limit for the year. This limit can’t be more than $9,250 in 2026 for in-network care, plus the cost of prescriptions.3

There is a great deal of variation in terms of plan design for Medicare Advantage plans. So the specifics of how your plan works, including the percentage that you pay in coinsurance, the services that are subject to coinsurance, and the out-of-pocket cap, will depend on the plan you choose.

Original Medicare doesn’t have a cap on how high a person’s coinsurance charges can be, as Original Medicare does not have a maximum out-of-pocket limit. This differs from virtually all other types of major medical coverage in the U.S., which are generally required to have out-of-pocket caps that don’t exceed $10,600 in 2026.4

As noted above, Medigap plans can help to cover some or all of the out-of-pocket costs that a person will have with Original Medicare, and Medicare Advantage plans are required to have a cap on in-network out-of-pocket costs that can’t exceed $9,250 in 2026 (plus the cost of prescription drugs).

Medicare provides broad coverage but doesn't cover everything. Original Medicare, for example, does not cover routine dental care, dentures, routine eye care, corrective lenses, dentures, hearing aids, or long-term nursing home care.

An overview of 2025 premiums and out-of-pocket costs for Original Medicare, Medicare Advantage, Medigap and Medicare Part D.

Medicare provides broad coverage but doesn't cover everything. Original Medicare, for example, does not cover routine dental care, dentures, routine eye care, corrective lenses, dentures, hearing aids, or long-term nursing home care.

An overview of 2025 premiums and out-of-pocket costs for Original Medicare, Medicare Advantage, Medigap and Medicare Part D.

Footnotes