You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

More than 33 million people have Original Medicare (Part A and Part B). Here’s a look at the benefits of 'traditional Medicare.'

Sometimes called “traditional Medicare,” Original Medicare is the fee-for-service program in which the government pays directly for healthcare costs that beneficiaries incur. Original Medicare became available in 1966, and consists of Part A and Part B.

Nearly 34 million people had Original Medicare as of April 2023. These enrollees can receive medical services anywhere in the country, as long as the medical provider accepts Medicare.

Most people become eligible for Original Medicare when they turn 65. But coverage is also available to younger people if they have a qualifying disability. Eligibility begins once they have been receiving Social Security disability benefits for two years. Younger people are also eligible if they’ve been diagnosed with Amyotrophic Lateral Sclerosis (ALS) or end-stage renal disease (ESRD). (See our article about Medicare eligibility based on ALS or ESRD.)

As of June 2024, more than 67.5 million people were enrolled in Medicare (roughly 33 million in Original Medicare and 34 million in Medicare Advantage). Of those enrollees, more than 7 million were under 65 and eligible due to a disability, ALS, or ESRD. The other 60 million people were 65 or older.1

Original Medicare covers most medically necessary care that beneficiaries need:

Most medical care is covered under Medicare Part A, Part B, or a combination of the two. But although Original Medicare may cover much of the care a typical beneficiary might need, there are some notable exceptions:

As we’ll discuss in the next section, there are also out-of-pocket costs associated with covered care under Original Medicare. So even for covered services, it’s important to understand that the enrollee may still have to pay some or all of the cost. (If it’s a service covered under Part B and the enrollee has not yet paid the Part B deductible, they would have to pay all of the charge if it’s less than the Part B deductible.)

Original Medicare costs include premiums (the amount you pay to have the coverage) and out-of-pocket costs (the amount you pay for a medical procedure). Here’s how those work for both parts of Original Medicare:

Part A 2025 premiums:

Part A is a $0 premium for about 99% of Medicare beneficiaries because they or a spouse paid Medicare taxes during at least 40 quarters of work history. For the other 1% of beneficiaries, the Part A monthly premium in 2025 is $285 if they have at least 30 quarters of work history, and $518 if they have less than 30 quarters of work history.2

Part A 2025 out-of-pocket expenses:

Part B 2025 premium:

For most beneficiaries, the Part B premium in 2024 is $185 a month.2 But some high-income beneficiaries pay more. (Learn more about this.) And on the other end of the income spectrum, some people are eligible for assistance that reduces or eliminates their Part B premiums. (See our state-by-state guide for more information about how this works.)

Part B 2025 out-of-pocket costs:

Part B has an annual deductible, which is $257 in 2025.2 After the beneficiary pays that amount, additional services covered by Part B are split 80/20, with Medicare paying 80% of the Medicare-approved amount, and the beneficiary paying the other 20%.

For most people, the answer to this seems to be yes. And indeed, most beneficiaries do have supplemental coverage.3

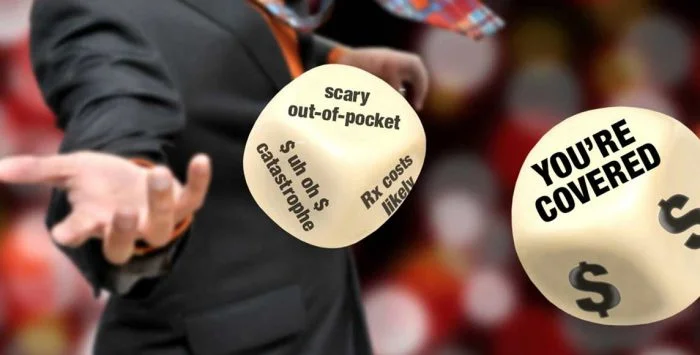

Supplemental coverage is optional, but it’s important to understand that Original Medicare does not have a cap on out-of-pocket costs. This includes the 20% Part B coinsurance, which can add up to an unlimited amount. Prior to enrolling in Medicare, many people are accustomed to health insurance that does have a limit on out-of-pocket costs. (For most plans, that limit can’t be more than $9,200 for in-network care in 2025, but that does not apply to Medicare.)

And Medicare Part A does not cover unlimited days in the hospital. A 60-day benefit period is enough to cover most hospitalizations. (The average inpatient stay is about five days.) But after an inpatient stay has reached 90 days, the beneficiary is limited to a lifetime maximum of 60 additional days of coverage under Original Medicare.

So in order to minimize out-of-pocket costs under Original Medicare, many beneficiaries maintain supplemental coverage, either through a Medigap policy or an employer/union/retiree policy. Medigap policies pay benefits after Medicare has paid its share, with different benefit levels depending on the plan the person selects. With employer/union/retiree coverage, the determination of which coverage is primary and which is secondary will depend on the size of the group health plan.

Since Original Medicare does not cover most outpatient prescription drugs, it’s also important for beneficiaries to maintain drug coverage, either from employer/union/retiree policy or Medicare Part D.

Choosing between Original Medicare and Medicare Advantage is a big decision, and there’s no right or wrong answer. But there are several points to keep in mind in terms of how they compare:

Original Medicare:

Medicare Advantage:

Explore plans from a licensed agency!

Eligibility for Medicare coverage depends on factors that include your work history, health status, and residency status. Check your eligibility today.

Learn how and when to enroll in Original Medicare, Medicare Advantage, Medigap, and Part D coverage. Get plan information and a free quote today.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

If your income is high or very low – or you're feeling lucky – you might be able to rely on traditional Medicare. Here's why most people don't.

Learn how premiums, out-of-pocket costs and income-related surcharges are changing for 2026 Medicare coverage.

Eligibility for Medicare coverage depends on factors that include your work history, health status, and residency status. Check your eligibility today.

Learn how and when to enroll in Original Medicare, Medicare Advantage, Medigap, and Part D coverage. Get plan information and a free quote today.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

If your income is high or very low – or you're feeling lucky – you might be able to rely on traditional Medicare. Here's why most people don't.

Learn how premiums, out-of-pocket costs and income-related surcharges are changing for 2026 Medicare coverage.

Footnotes