You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

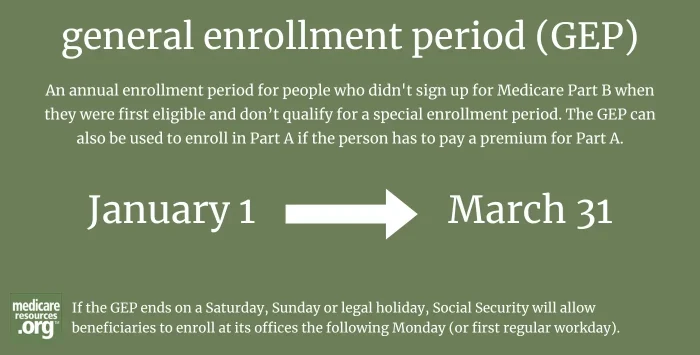

Medicare’s general enrollment period (GEP) is an annual opportunity for certain eligible individuals to enroll in Medicare Part A and/or Medicare Part B.

The general open enrollment period runs from January 1 through March 31 each year. If the GEP ends on a Saturday, Sunday or legal holiday, Social Security will allow beneficiaries to enroll at its offices the following Monday (or first regular workday). In addition to in-person enrollment, Social Security will honor a written enrollment request if it’s stamped by the last day of the GEP.

A Medicare-eligible person can enroll in Medicare Part B during the GEP if they didn’t enroll during their initial enrollment period or during a Part B special enrollment period (SEP). Beneficiaries who have to pay a premium for Medicare Part A are allowed to sign up for Part A during the GEP, if they didn’t enroll during their initial enrollment period (most people do not have to pay a premium for Part A, so they can enroll in it at any time once they’re Medicare-eligible).

It’s best to sign up for Part B during your initial enrollment period or Part B special enrollment period (SEP). But if you don’t enroll during either of those times, you can sign up during the GEP and your coverage will take effect the first of the following month.

Prior to 2023, there was a delayed effective date for GEP enrollments: Regardless of when a person signed up during the GEP, coverage would begin July 1 and the person’s Part B coverage would start July 1. But as of 2023 – under a rule change that CMS initiated in order to comply with legislation that was enacted in 2020 – there will no longer be a delayed effective date for GEP enrollments. Instead, coverage will simply take effect the first of the month following enrollment. So, a person who enrolls in January will have coverage effective in February, instead of having to wait until July.

If you went at least a year without Part B (and/or Part A, if you have to pay a premium for it) after you were initially eligible to enroll, you may owe a late enrollment penalty. The penalty does not apply if you qualify for a Part B special enrollment period. But if you’re enrolling during the GEP, you may find that you owe a penalty.

The penalties are different for Part A and Part B:

Learn more: Can I get a Medicare late enrollment penalty removed?

If you qualify for premium-free Part A, you can enroll in it at any time. But if you have to pay a premium for Part A (also called “buying” Part A), you have to sign up for Part A either during your initial enrollment period that starts three months before your 65th birthday or during the GEP.

If you’re paying a premium for Part A and you enroll during the GEP, coverage effective dates are the same as for Part B – meaning that as of 2023, your coverage begins the month after you enroll. As is the case with Part B, if you have to buy Part A and delayed enrolling until after you were first eligible, you’ll probably owe a late-enrollment penalty.

Medicare beneficiaries need to know when their plan will be effective so they can avoid coverage gaps that could leave them without access to care they need.

Medicareresources.org announced today the release of its 2022 Medicare Open Enrollment Guide and provided five tips for evaluating and selecting Medicare coverage.

The Medicare Part B SEP allows people to delay Part B enrollment if they have health coverage through their own employer or a spouse’s current employer.

Medicare beneficiaries need to know when their plan will be effective so they can avoid coverage gaps that could leave them without access to care they need.

Medicareresources.org announced today the release of its 2022 Medicare Open Enrollment Guide and provided five tips for evaluating and selecting Medicare coverage.

The Medicare Part B SEP allows people to delay Part B enrollment if they have health coverage through their own employer or a spouse’s current employer.