You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

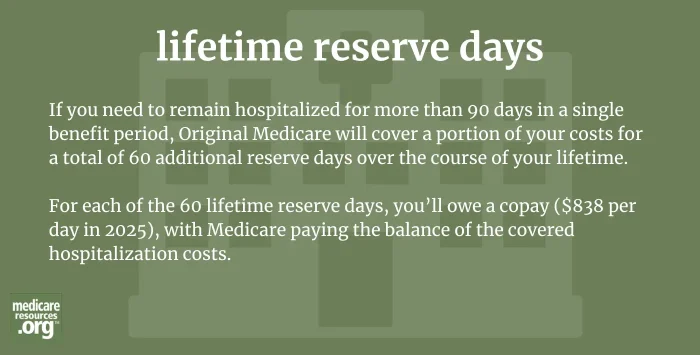

If you need to remain hospitalized for more than 90 days in a single benefit period, Original Medicare will cover a portion of your costs for a total of 60 additional reserve days over the course of your lifetime. For each of these 60 lifetime reserve days, you’ll owe a copay of $838 per day in 2025,1 and Medicare pays the rest of the covered hospital costs.

Medicare inpatient coverage is based on how long you’re hospitalized. When you’re first admitted as an inpatient at the start of your benefit period, you pay your deductible ($1,676 in 20252), and then Medicare pays for your inpatient care for 60 days, without you having to pay anything else for inpatient care.

If you’re still hospitalized after 60 days, you’ll start paying a portion of the bill, for the next 30 days. In 2025, you’ll pay $419 for each day in the hospital from day 61 to day 90.2

If you’re still hospitalized after 90 days, you’ll start dipping into your lifetime reserve days. If you use lifetime reserve days, you pay $838 per day in 2025 and Medicare pays the rest. If you’re ultimately discharged from the hospital after a total of 100 days, you will have used up 10 of your lifetime reserve days. That means you’ll have 50 remaining, which you could use in the future if you ever have another hospitalization that lasts more than 90 days.

If you buy a Medigap policy, it will pay your hospital coinsurance costs, and will also cover an extra 365 days of inpatient coverage, after your Medicare lifetime reserve days are used up. If you have supplemental coverage from a current or former employer, the benefit details will depend on the plan, so it’s important to understand how your plan would cover your costs if you were to have an extended inpatient stay.

Alternatively, Medicare Advantage plans have built-in caps on out-of-pocket costs, which can’t exceed $9,350 for in-network care (not counting prescription drug costs) in 2025.3

So with a Medicare Advantage plan, it doesn’t matter how many days you’re hospitalized — you won’t have to pay more than the plan’s out-of-pocket limit for your hospitalization. But this is only true as long as the plan considers your ongoing care to be medically necessary and you and your medical team comply with any prior authorization requirements the plan has. (This article will help you figure out whether you’d be better off with Medicare Advantage or Original Medicare.)

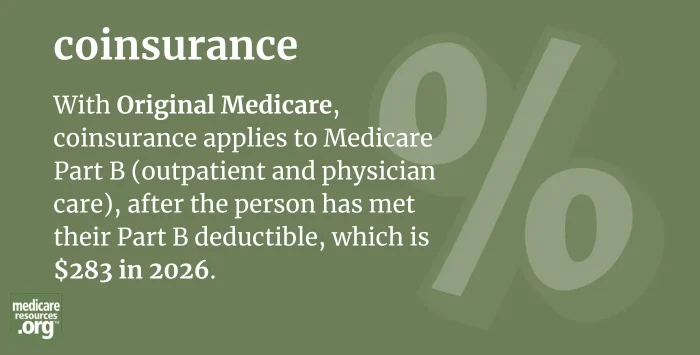

Coinsurance refers to a percentage of the Medicare-approved cost of your health care services that you're expected to pay after you've paid your plan deductibles.

If your income is high or very low – or you're feeling lucky – you might be able to rely on traditional Medicare. Here's why most people don't.

Coinsurance refers to a percentage of the Medicare-approved cost of your health care services that you're expected to pay after you've paid your plan deductibles.

If your income is high or very low – or you're feeling lucky – you might be able to rely on traditional Medicare. Here's why most people don't.

Footnotes