You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Minneapolis, MN – Based on early indicators, some Medicare beneficiaries may see double-digit increases in their prescription drug premiums and higher out-of-pocket costs in 2024, according to medicareresources.org.

Medicare open enrollment – also known as the Medicare annual election period (AEP) – begins Oct. 15 and closes Dec. 7. It is the time when millions of Medicare enrollees can switch from Original Medicare to Medicare Advantage, or vice versa, and make changes to their Medicare Advantage plans or Medicare Part D prescription drug plans (Part D). This includes dropping or enrolling in stand-alone Medicare Part D prescription drug plans. Read our guide to Medicare enrollment.

“Many consumers don’t review their plans during Medicare open enrollment but, especially this year, that could be a costly mistake,” said Jenny Chumbley Hogue, an analyst for medicareresources.org. “There are several important developments that may impact people’s coverage and how much they pay.”

Here are three important things to know:

About 50 million Medicare beneficiaries receive prescription drug coverage through Medicare Part D prescription drug plans. Medicare Part D coverage includes either a stand-alone prescription drug plan– which covers only prescription drugs – or a Medicare Advantage plan with integrated Part D coverage, which covers prescriptions and other medical expenses.

The Biden Administration recently made headlines with a list of drugs that will be subject to price negotiations, as recent legislation now allows Medicare to negotiate prices with drug manufacturers. But consumers who use these medications will not experience the full impact of those negotiations until 2026.

In fact, some consumers in stand-alone Part D plans may see large premium increases in 2024.

“It will depend on the prescription drug plan, but we anticipate that while some carriers will decrease their premiums, others will nearly double their rates,” Chumbley Hogue said. “The bottom line is consumers should not assume their coverage will stay the same in 2024.”

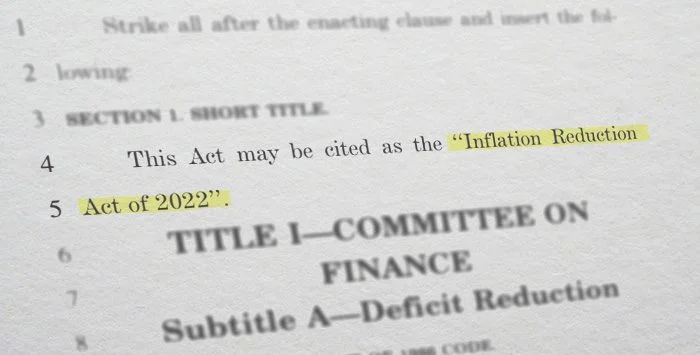

The Inflation Reduction Act (IRA) passed in 2022 will provide relief for 1.5 million Medicare beneficiaries who have very high drug costs. Historically, this high-needs group has paid 5% coinsurance (or any copays) after their drug spending reached a certain level. Beginning in January 2024, enrollees who reach this “catastrophic coverage” level will no longer pay out-of-pocket costs for drugs that are covered by their Part D plan.

Additionally, the IRA will cap annual base beneficiary premium increases at 6%, starting in 2024. However, the base beneficiary premium is just one factor in how premiums are calculated. So while this does have the effect of keeping Part D premiums lower than they would otherwise have been, the actual rate changes that enrollees will see in 2024 will vary considerably, and are not capped.

Medicareresources.org analysts predict that enrollment in these plans will continue to grow in 2024. Medicare Advantage plans can offer significant savings on prescription drugs, as well as additional benefits such as dental, hearing and vision coverage. This year, 30.8 million people – more than half of all eligible Medicare beneficiaries – are enrolled in Medicare Advantage plans. That’s remarkable growth since the program first launched around 2004, when just 13% of Medicare beneficiaries had Medicare Advantage.

But Medicare Advantage plans also come with limitations that people should familiarize themselves with before signing up. For example, unlike Original Medicare, most Medicare Advantage plans limit enrollees to a specific network of providers. And enrollees should know that if they opt for Medicare Advantage and then decide more than a year later that they’d rather have Original Medicare, their access to Medigap (Medicare supplemental) coverage will likely depend on their medical history.

“This year comes with lots of changes, and it’s a good idea to review plans during open enrollment,” said Louise Norris, health policy analyst for medicareresources.org. “No one wants to be surprised by unexpected costs after their coverage begins.”

Medicareresources.org has been an online source of in-depth information about Medicare for consumers since 2011. The site, owned by HealthInsurance.org, LLC, provides an overview of the basics of Medicare coverage options, enrollment and eligibility; coverage FAQs; state-specific Medicare information; and a glossary of Medicare terms. Medicareresources.org is not connected with or endorsed by the U.S. government or the federal Medicare program.

Contact:

Amy Fletcher Faircloth, [email protected]

Beginning in 2023, a series of changes began to be phased in under the Inflation Reduction Act, designed to lower out-of-pocket costs, expand access to vaccines, and rein in drug price increases.

Medicare enrollees do not have to pay a deductible, copay, or coinsurance to get the shingles vaccine. The vaccine will be free whether a beneficiary is enrolled in a stand-alone Part D plan or a Medicare Advantage plan with drug coverage included.

Beginning in 2023, a series of changes began to be phased in under the Inflation Reduction Act, designed to lower out-of-pocket costs, expand access to vaccines, and rein in drug price increases.

Medicare enrollees do not have to pay a deductible, copay, or coinsurance to get the shingles vaccine. The vaccine will be free whether a beneficiary is enrolled in a stand-alone Part D plan or a Medicare Advantage plan with drug coverage included.