You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

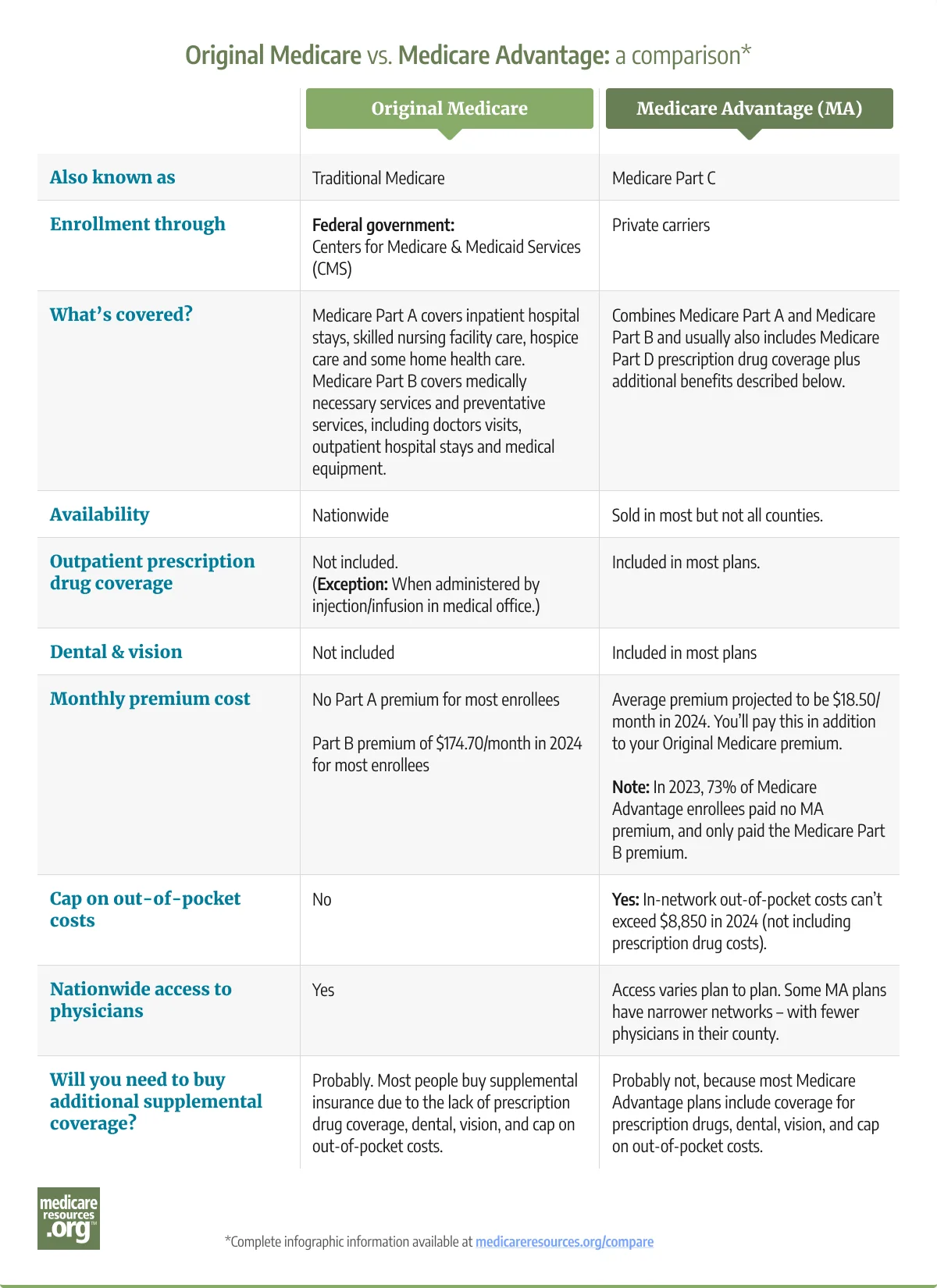

Minneapolis – With Medicare open enrollment underway, it’s helpful for consumers to understand the difference between Original Medicare and Medicare Advantage. Today, medicareresources.org offered tips and a new infographic to help people compare coverage and possibly save money.

Medicare open enrollment – also known as the annual election period – ends Dec. 7. During the open enrollment period, millions of Medicare enrollees can:

“As beneficiaries compare different Medicare plans, they may be confused by the differences or overwhelmed by all the options,” said Louise Norris, a health policy analyst for medicareresources.org. “But that shouldn’t stop them from doing the research. Comparing plans during Medicare open enrollment really can help consumers save money.”

“It’s hard to overemphasize how many Americans are potentially impacted by open enrollment season,” Norris added.

“Of approximately 60 million eligible Medicare beneficiaries, 51% are enrolled in Medicare Advantage plans in 2023 – a significant jump from the 19% enrolled in 2007, according to KFF,” Norris said.

Here are a few things to consider when deciding between Original Medicare versus Medicare Advantage, or pairing Original Medicare with a Medigap or Part D plan.

In most areas, there are “zero-premium” Medicare Advantage plans available. However, enrollees who buy these plans still must pay the Medicare Part B premium, which is $174.70 a month for most enrollees in 2024.

People who opt for Original Medicare with supplemental coverage – assuming they don’t have supplemental coverage from Medicaid or an employer-sponsored plan — will pay a Medigap and/or Part D premium in addition to the Part B premium.

The average premium for a stand-alone Part D plan in 2024 is projected by KFF to be $48/month based on current enrollment, but expected to be less than that once enrollees finalize their plan selections for 2024. And as is always the case, premiums vary widely from one plan to another.

“Zero-premium Medicare Advantage plans can be attractive for some people,” Norris said. “But while Original Medicare paired with Medigap coverage may come with a higher monthly premium, the supplemental coverage could substantially lower out-of-pocket costs, and the Original Medicare and Medigap combination will allow access to a larger number of medical providers.”

With most Medicare Advantage plans, beneficiaries will pay a deductible, coinsurance and/or copays, and the out-of-pocket maximum can be as high as $8,850 in 2024 for services covered under Medicare Parts A and B. Also, people with Medicare Advantage plans will have additional out-of-pocket costs for prescription drugs. Most Medicare Advantage plans do cover prescription drugs, but the out-of-pocket costs are not applied to the regular medical out-of-pocket limit.

If people pair Original Medicare with Medigap, there are plans available that pay nearly first-dollar coverage for all Original Medicare-covered services, leaving enrollees with potentially very little in out-of-pocket costs other than the cost of medications under Medicare Part D. The most comprehensive Medigap plans tend to be among the more expensive options. Less-expensive options leave enrollees with varying amounts of out-of-pocket costs for services that are covered by Original Medicare.

When exploring plans, also consider the provider network, extra benefits and how care will be covered if you travel:

“Plan details can change from year to year,” Norris said. “Even if you’re satisfied with your existing coverage, it’s worth comparing plans since plan details can change from year to year.”

Find more detailed information about Medicare open enrollment in our Medicare Open Enrollment Guide.

Medicareresources.org has been an online source of in-depth information about Medicare for consumers since 2011. The site, owned by HealthInsurance.org, LLC, provides an overview of the basics of Medicare coverage options, enrollment and eligibility; coverage FAQs; state-specific Medicare information; and a glossary of Medicare terms. Medicareresources.org is not connected with or endorsed by the U.S. government or the federal Medicare program.

Contact:

Amy Fletcher Faircloth, [email protected]

{kind=link}