You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Modern Medigap plans do not include prescription drug benefits. Instead, Medicare offers prescription drug coverage under Part D. Medicare enrollees can get prescription coverage either by switching to a Medicare Advantage plan (almost all of them include prescription coverage)1 or by purchasing a stand-alone Medicare Part D plan (PDP) to go along with Original Medicare.

However, if you purchased a Medigap policy prior to January 1, 2006 and still have the same plan, it may include prescription drug coverage. Plans H, I, and J included limited prescription coverage for beneficiaries who purchased them prior to 2006, although those plans are no longer sold.

If you’re in this situation and you want to join a PDP, you must drop the prescription drug coverage from your Medigap since you can’t have two separate prescription drug coverage policies at the same time.2

You can drop just your Medigap prescription coverage and keep the other coverage provided by your current Medigap plan. And you’ll have the option to enroll in a Part D plan during the annual Medicare open enrollment period that runs from October 15 to December 7. But you’ll have to pay a late enrollment penalty for Part D, if the Medigap plan has been providing your only prescription drug coverage and it didn’t qualify as creditable coverage.3

Your Medigap plan can tell you whether the drug benefits it provides are creditable,2 but CMS noted in 2005 that “Plans H and I would never meet the definition of creditable coverage and that Plan J was unlikely to.”4

Although there was a guaranteed issue period in 2005/2006 for people with pre-2006 Medigap plans to switch to a new Medigap plan and also enroll in a PDP,2 if you’re doing that now, you’ll probably have to go through medical underwriting for the Medigap plan (unless you qualify for a guaranteed issue right, or live in a state where Medigap plans don’t use medical underwriting or have annual plan change windows available).

If you didn’t enroll in Part D when you were first eligible and instead relied on drug coverage that wasn’t considered creditable, you’ll owe a late enrollment penalty if and when you eventually switch to a Part D plan.

As noted above, CMS did not expect Medigap drug coverage to be considered creditable. So it’s likely that if you’ve kept Medigap Plan H, I, or J and used that plan’s drug coverage, you’ll owe a late enrollment penalty if you’re switching to Part D.

The penalty is 12% for each year that enrollment was delayed and is calculated in one-month increments. It is based on the nationwide base Part D premium, so your penalty won’t be higher if you enroll in a more expensive plan.3

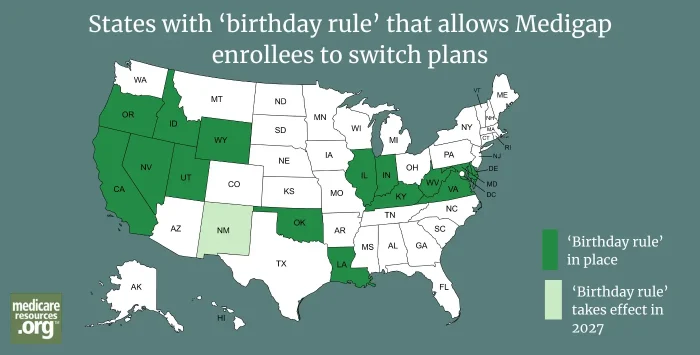

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

We asked how confident our readers were with comparison shopping for a Medicare Part D plan during the 2022 Medicare Annual Enrollment Period. Here's what we learned from more than 350 survey responses.

Reasons to consider a change to your Medicare prescription drug coverage may include high premiums, changes to your prescriptions or your plan's formulary, and your access to in-network pharmacies.

Prescription drugs – and drug coverage – can be less expensive if you're willing to do a little research and to reach out for help. Here are eight strategies that will empower you to take control of your drug coverage and your medication costs.

The best time to enroll in a Medicare supplement plan is during your Medigap open enrollment period, a six-month window that begins on the first of the month you're enrolled in Medicare Part B and are 65 or older.

Medicare supplement insurance, or Medigap, is insurance that supplements Original Medicare, covering some or all of the out-of-pocket costs that a beneficiary would otherwise have to pay for services covered by Original Medicare.

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

We asked how confident our readers were with comparison shopping for a Medicare Part D plan during the 2022 Medicare Annual Enrollment Period. Here's what we learned from more than 350 survey responses.

Reasons to consider a change to your Medicare prescription drug coverage may include high premiums, changes to your prescriptions or your plan's formulary, and your access to in-network pharmacies.

Prescription drugs – and drug coverage – can be less expensive if you're willing to do a little research and to reach out for help. Here are eight strategies that will empower you to take control of your drug coverage and your medication costs.

The best time to enroll in a Medicare supplement plan is during your Medigap open enrollment period, a six-month window that begins on the first of the month you're enrolled in Medicare Part B and are 65 or older.

Medicare supplement insurance, or Medigap, is insurance that supplements Original Medicare, covering some or all of the out-of-pocket costs that a beneficiary would otherwise have to pay for services covered by Original Medicare.

Footnotes