You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Here’s a look at several changes to Medicare prescription drug coverage taking effect in 2026:

Under the Inflation Reduction Act, Medicare Part D has a cap on out-of-pocket costs. In 2025, enrollees paid no more than $2,000 in out-of-pocket costs for their covered drugs.1 But that limit is subject to inflation adjustment, and it’s increasing to $2,100 in 2026.2

As was the case in 2025, enrollees will continue to have the option to spread their drug costs out in equal payments across the year. This could be beneficial to those who might otherwise have to pay the full $2,100 in just the first few months of the year.3

Various other improvements to Medicare Part D benefits (and coverage of drugs under Part B) have been phased in since 2023 as a result of the Inflation Reduction Act. These include $35 insulin, free recommended vaccines, and lower coinsurance costs for certain infusion drugs covered under Medicare Part B. These provisions continue to be in place in 2026.

Suggested: Does Medicare cover the shingles vaccine?

The Part D prescription drug deductible was a maximum of $590 in 2025,4 and that cap is increasing to $615 in 2026.5

Some Part D plans have deductibles well under these amounts (or no deductible at all), but no plans can have deductibles that exceed $615 in 2026.

After you pay your deductible, you’ll pay copays (a fixed amount) or coinsurance (a percentage of the cost) for your medications until you’ve spent $2,100 in out-of-pocket costs. After that, your covered drugs will have no out-of-pocket costs for the rest of the year.

It’s important to mention that changes to your Medicare Part D costs can stem from changes in your own prescription needs, changes in your plan’s design, or a plan change that you make during open enrollment (October 15 – December 7). It’s important to carefully compare the various options each year during open enrollment to see how your existing plan – and the other plans available in your area – will cover your specific drugs for the coming year.

This is true whether your Part D coverage is provided by a stand-alone plan or as part of a Medicare Advantage plan. But if you have a Medicare Advantage plan, you’ll also need to consider how the plan and available alternatives cover the rest of your medical needs, in addition to your prescription needs.

(Medicare’s plan comparison tool is useful for determining how each plan will cover your prescription drugs, and what your out-of-pocket costs will be. If in doubt, it’s important to seek assistance from a broker or SHIP counselor, or to call Medicare or the health plan directly.)

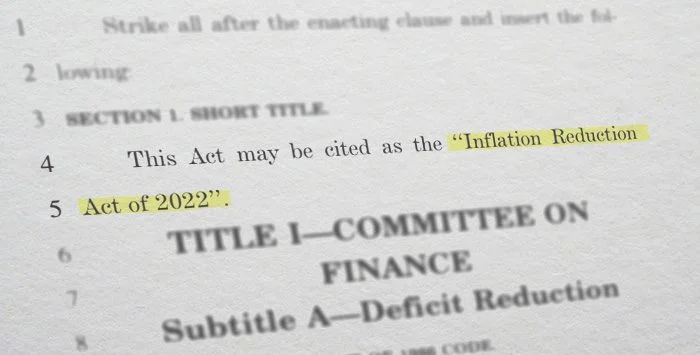

The Inflation Reduction Act allowed Medicare to begin price negotiations with drug manufacturers, which previously wasn’t allowed.6 The price negotiations are being phased in over several years.

Ten drugs – covered by Medicare Part D – were selected for the first round of negotiations, and their negotiated prices take effect in January 2026. Negotiated prices apply to Januvia, Fiasp/NovoLog, Farxiga, Enbrel, Jardiance, Stelara, Xarelto, Eliquis, Entresto, and Imbruvica.7

Enrollees who take medications with newly negotiated prices might find that they pay lower copays or coinsurance when they fill those prescriptions in 2026. And the $2,100 Part D out-of-pocket cap will protect enrollees whose costs would otherwise exceed that limit.

Another 15 drugs will have negotiated prices starting in 2027: Ozempic, Rybelsus, Wegovy, Xtandi, Pomalyst, Ibrance, Calquence, Trelegy Ellipta, Ofev, Breo Ellipta, Vraylar, Janumet, Otezla, Linzess, and Xifaxan.8

Learn more about the Medicare drug price negotiation program.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written hundreds of opinions and educational pieces about the Affordable Care Act and Medicare for healthinsurance.org and medicareresources.org.

The Inflation Reduction Act – passed in August 2022 – was designed to decrease how much Medicare enrollees have to spend on diabetes care.

Beginning in 2023, a series of changes began to be phased in under the Inflation Reduction Act, designed to lower out-of-pocket costs, expand access to vaccines, and rein in drug price increases.

Reasons to consider a change to your Medicare prescription drug coverage may include high premiums, changes to your prescriptions or your plan's formulary, and your access to in-network pharmacies.

Prescription drugs – and drug coverage – can be less expensive if you're willing to do a little research and to reach out for help. Here are eight strategies that will empower you to take control of your drug coverage and your medication costs.

Medicare reimbursement refers to the payments that hospitals and physicians receive in return for services rendered to Medicare beneficiaries. The reimbursement rates for these services are set by Medicare, and are typically less than the amount billed or the amount that a private insurance company would pay.

If you're like most Medicare enrollees, you probably aren't planning to make any changes to your existing coverage for the coming year, but – like most beneficiaries – you should probably at least consider it during Medicare's open enrollment period. And if you have Medicare Advantage, you also have an opportunity to change your coverage between January and March each year.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

The Inflation Reduction Act – passed in August 2022 – was designed to decrease how much Medicare enrollees have to spend on diabetes care.

Beginning in 2023, a series of changes began to be phased in under the Inflation Reduction Act, designed to lower out-of-pocket costs, expand access to vaccines, and rein in drug price increases.

Reasons to consider a change to your Medicare prescription drug coverage may include high premiums, changes to your prescriptions or your plan's formulary, and your access to in-network pharmacies.

Prescription drugs – and drug coverage – can be less expensive if you're willing to do a little research and to reach out for help. Here are eight strategies that will empower you to take control of your drug coverage and your medication costs.

Medicare reimbursement refers to the payments that hospitals and physicians receive in return for services rendered to Medicare beneficiaries. The reimbursement rates for these services are set by Medicare, and are typically less than the amount billed or the amount that a private insurance company would pay.

If you're like most Medicare enrollees, you probably aren't planning to make any changes to your existing coverage for the coming year, but – like most beneficiaries – you should probably at least consider it during Medicare's open enrollment period. And if you have Medicare Advantage, you also have an opportunity to change your coverage between January and March each year.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

Footnotes