You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

When you have surgery, there are bills for more than just the surgery itself. There are also bills for anesthesiology services, facility fees to use the operating suite, and of course, the surgeon’s fees and possibly an assistant surgeon’s fees. If you’re inpatient, there’s also the care you receive in the hospital after surgery – nursing care, tests such as lab work or X-rays, medications, and physical therapy, if you need it – all of which add to the total bill.

Many people assume their insurance is going to cover these expenses. But when it comes to Medicare, how much you pay out of pocket will depend on whether Medicare Part A or Medicare Part B picks up the tab.

While Part A is known as “hospital insurance,” it’s actually not enough for you to simply be in the hospital for your Part A coverage to kick in.

In 2013, CMS enacted what is known as the two-midnight rule.1 This rule added a clock to the admission process for hospital stays. Not only do you have to have medical reasons to stay in the hospital, but your doctor also has to deem you sick enough that your hospital stay would likely cross two midnights (with exceptions for certain surgeries, described below).

Only when both these criteria are met would a patient be considered appropriate for Part A “inpatient” coverage. Otherwise, you would be considered an “outpatient” and would be placed under observation. In that case, Part B covers any care received. (Starting in 2024, CMS began requiring Medicare Advantage plans to also adhere to the two-midnight rule.)2

If you’re approved for inpatient coverage under Part A, you would pay a fixed deductible amount for most of the services you receive during the hospital stay (a $1,736 Part A deductible in 2026 covers you up to 60 days),3 plus, for any physician services you receive, the Part B deductible ($283 in 2026) and 20% of the cost of those physician services (billed under Part B). If you have a Medicare Advantage plan, the cost-sharing will depend on your plan, as these policies vary considerably in terms of deductibles, coinsurance, and out-of-pocket caps.

But if your care is not approved for inpatient status, you would be charged the Part B deductible and then 20% of the cost of each individual service you received – up to and including room and board. It’s important to point out that your costs under Part B for any one hospital service cannot be more than the Part A deductible. But your total costs under Part B can certainly add up to more than the Part A deductible.4

Even when you receive the very best medical care, you may still need time to recover after a hospitalization.

You could receive that care at home, in the form of physical therapy or other home services, for example. In those cases, you will turn to your Part B coverage.

Other times, you may require placement in a skilled nursing facility (SNF) for intensive rehab. If your hospital care was considered inpatient and lasted at least three days, Medicare Part A will pay for your SNF rehab, and you won’t have any additional costs for the first 20 days of that care. You’ll also have Part A coverage for up to 80 additional SNF days, but with a copay of $217 per day in 2026.3

However, Part A won’t cover your stay in a skilled nursing facility unless you have had inpatient orders on your medical record for at least three days, not counting the day you are transferred to the SNF. So if your hospital stay was classified as observation rather than inpatient (covered by Part B rather than Part A), you won’t have any Medicare coverage for the subsequent SNF rehab stay.5

While going under the knife is not always something you want to do, it may be something you need to do. Millions of elective (non-emergency) surgeries are performed each year. If your surgery is done in a hospital rather than an outpatient clinic (or hospital outpatient department), your admission status – inpatient or observation – could significantly impact how much you pay for those surgeries.

Every year, CMS releases a list of “inpatient only” (IPO) surgeries it considers to be inpatient appropriate. Because these surgeries are considered higher risk, they are automatically covered by Medicare Part A. In those cases, your stay does not need to meet the expectation that it will cross two midnights.

However, CMS has started to trim its IPO list. In 2018, it removed total knee replacements from the list. In 2020, it removed total hip replacements. CMS planned to phase out the list altogether by 2024, but this decision was put on hold and delayed. CMS announced in 2025 that the IPO list would be phased out over three years, starting in 2026, although the future of this plan also depends on stakeholder feedback.6

To be clear, the reason CMS plans to phase out the IPO list is because of evolving clinical practices that make an increasing number of surgeries safe and effective as outpatient procedures. But there are still concerns about patient safety when surgeries are performed on an outpatient basis, so there is ongoing debate on this issue.

From a consumer perspective, if you have Original Medicare and your surgery is scheduled to take place in a hospital (with you staying overnight in the hospital, rather than using the hospital outpatient department and going home after the surgery), it’s important to discuss the details with your care team, and find out whether you’re being admitted as an inpatient. If so, you can expect to pay your Part A deductible plus Part B costs for any physician services you receive. If not, you can expect to pay the Part B deductible plus 20% of the cost of all services you receive, and you will not be eligible for Medicare coverage of SNF rehab. Discussing this in advance with your care team and the hospital billing department can help to prevent surprise bills after the fact.

Yes. Your costs might not be affected if you have an uncomplicated surgery and go home the same day or even the day after – especially if your hospital bundles payments. However, a longer hospital stay under observation status could affect your bottom line.

Having a surgery that is not on the inpatient-only list does not mean your doctor cannot admit you as an inpatient, whether it’s on the day of the surgery or a following day. Your doctor must clearly document why your hospital stay was more complicated or higher risk than the average surgery course. Otherwise, Medicare could deny Part A coverage, sweeping you into a long appeals process.

Most Medicare beneficiaries have either Medicare Advantage (with or without additional coverage) or supplemental coverage that will pick up the tab for some or all of the Original Medicare out-of-pocket costs that beneficiaries would otherwise have to pay themselves.7

If you aren’t eligible for Medicaid or coverage from a current or former employer, you can choose to enroll in a Medigap plan to supplement Original Medicare. In most areas of the country, you also have the option of a Medicare Advantage plan instead of Original Medicare. Learn more about choosing between the various Medicare coverage options.

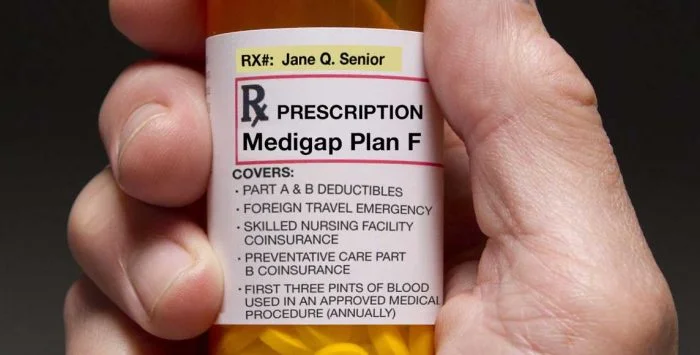

Most Medigap plans will eliminate the worry over whether your hospital stay is paid under Part A or Part B. That’s because they’ll cover the Part A deductible and any Part B coinsurance that you incur. (Some Medigap plans – A, K, L, and M, as well as the high-deductible versions of Plan F and G – will still leave you with some out-of-pocket costs.)

If you’d rather have a Medicare Advantage plan, it will take the place of Original Medicare, with both Part A and Part B wrapped into one private plan that will likely also include Part D prescription coverage and various extra benefits. And unlike Original Medicare, there is a cap on out-of-pocket costs for Part A and Part B benefits under Medicare Advantage plans. (Annual costs can’t exceed $9,250 in 2026,8 although most plans tend to have out-of-pocket limits well below this.9 (Note that the Medicare Advantage out-of-pocket limit does not include the cost of premiums, and it also does not include the cost of prescription drugs, which have a separate $2,100 out-of-pocket limit in 2026.)10

Like most commercial payers, Medicare Advantage plans typically require prior authorization for elective surgery.11 In that case, you would know before you even set foot in the door if your surgery was approved for inpatient or observation coverage.

Also, Medicare Advantage plans have the option of waiving the three-day rule for skilled nursing facility coverage.5 This could offer significant savings if you were to need extended care after your surgery.

Although the specifics vary from one plan to another, you’ll generally have higher out-of-pocket costs under Medicare Advantage than you’d have with Original Medicare plus Medigap, and you’ll likely need to obtain prior authorization before having any elective surgery, and stay within your plan’s provider network. But premiums also tend to be lower with Medicare Advantage, so there’s no right or wrong answer.

Tanya Feke, M.D. is a licensed, board-certified family physician living in New Hampshire. As a practicing primary care physician in Connecticut and an urgent care physician in New Hampshire, she saw first-hand how Medicare impacted her patients. In recent years, her career path has shifted to consultant work with a focus on utilization management and medical necessity compliance.

Dr. Feke is an expert in the field, having Medicare experience on the frontlines with patients, hospital systems, and insurers. To educate the public about ongoing issues with the program, she authored “Medicare Essentials: A Physician Insider Reveals the Fine Print.” Her analysis of Medicare issues is frequently referenced by the media, and she is a contributor to multiple online publications.

Medicare provides broad coverage but doesn't cover everything. Original Medicare, for example, does not cover routine dental care, dentures, routine eye care, corrective lenses, dentures, hearing aids, or long-term nursing home care.

As a Medicare enrollee, you'll face a range of out-of-pocket costs. When you know what to look for, you can find ways to minimize these costs and protect yourself.

Considering a change to your Medicare coverage? Consider these 10 factors when choosing between Medicare Advantage, Medigap, and Part D coverage.

Medicare provides broad coverage but doesn't cover everything. Original Medicare, for example, does not cover routine dental care, dentures, routine eye care, corrective lenses, dentures, hearing aids, or long-term nursing home care.

As a Medicare enrollee, you'll face a range of out-of-pocket costs. When you know what to look for, you can find ways to minimize these costs and protect yourself.

Considering a change to your Medicare coverage? Consider these 10 factors when choosing between Medicare Advantage, Medigap, and Part D coverage.

Footnotes