You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

The Minimum Monthly Maintenance Needs Allowance, or MMMNA, refers to the fact that if one spouse is receiving Medicaid-funded long-term services and supports (LTSS) in a nursing home or via Medicaid’s Home and Community-Based Services, the other spouse might be allowed to keep some or all of the Medicaid-covered spouse’s income.

In most cases, only the income of the spouse receiving LTSS is counted toward the eligibility limit for Medicaid long-term care benefits. But if the other spouse (known as the “community spouse” or “well-spouse”) has little or no income of their own, they will be allowed to keep some of their spouse’s income via the MMMNA. These rules are designed to protect the community spouse from becoming impoverished so that their spouse can qualify for Medicaid.

If a community spouse’s monthly income is below a certain amount, they can keep a Minimum Monthly Maintenance Needs Allowance from the income of their spouse who receives nursing home or HCBS benefits – which can increase a community spouse’s income until it reaches that amount. This is sometimes called a “spousal allowance.” This ensures that if the spouse who needs Medicaid LTSS is the breadwinner, the other spouse will not be left without an income.

The MMMNA varies in each state and is indexed annually. In 2025, it can range from a minimum of about $2,644/month to a maximum of $3,948/month, in the continental United States (higher in Alaska and Hawaii).1

People with Medicare and Medicaid are known as dual eligibles – and account for about 20 percent of Medicare beneficiaries (12.1 million people). Learn how that status affects your coverage.

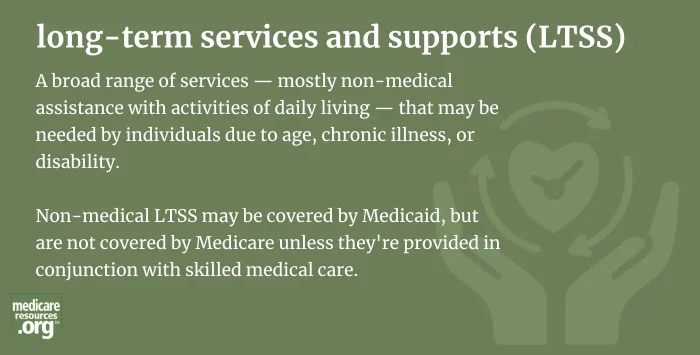

The term long-term services and supports (LTSS) encompasses an array of medical and personal care services for people who struggle with self-care due to aging, illness or disability. People commonly receive LTSS services for months or even years (and this is why LTSS are sometimes referred to as “long-term care”).

In 2016, an estimated 11.7 million Medicare beneficiaries – about 20 percent of all enrollees – were also enrolled in Medicaid and are known as dual-eligible beneficiaries or dual-eligibles. And while you might not hear that term often – or at all – it's worth your time to understand what it means to have both Medicare and Medicaid (especially if you or a loved one is part of the "Medicare-Medicaid" population).

People with Medicare and Medicaid are known as dual eligibles – and account for about 20 percent of Medicare beneficiaries (12.1 million people). Learn how that status affects your coverage.

The term long-term services and supports (LTSS) encompasses an array of medical and personal care services for people who struggle with self-care due to aging, illness or disability. People commonly receive LTSS services for months or even years (and this is why LTSS are sometimes referred to as “long-term care”).

In 2016, an estimated 11.7 million Medicare beneficiaries – about 20 percent of all enrollees – were also enrolled in Medicaid and are known as dual-eligible beneficiaries or dual-eligibles. And while you might not hear that term often – or at all – it's worth your time to understand what it means to have both Medicare and Medicaid (especially if you or a loved one is part of the "Medicare-Medicaid" population).

Footnotes