You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

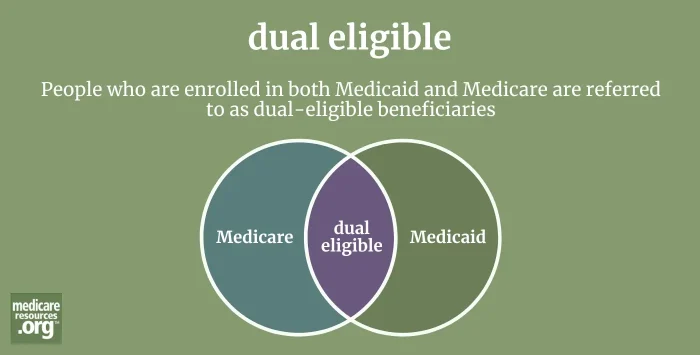

If you’re familiar at all with Medicare, you know that while the program promises healthcare security for millions – including the vast majority of Americans age 65 and older – Medicare is also riddled with coverage gaps.

Since Medicare was passed into law, a range of private coverage options – Medicare Advantage, Medigap, and Medicare Part D – were created to help enrollees deal with those coverage gaps and manage the program’s costs. But today, a vast cross-section of Medicare enrollees also receives coverage and financial support through another well-known safety net: Medicaid.

As of 2019, an estimated 12.3 million Medicare beneficiaries – about 19% of all enrollees – were also enrolled in Medicaid or a Medicaid-funded program. These enrollees are known as dual-eligible beneficiaries or dual-eligibles. And while you might not hear that term often – or at all – it’s worth your time to understand what it means to have both Medicare and Medicaid (especially if you or a loved one is part of the “Medicare-Medicaid” population).

If you’re enrolled in both Medicaid and Medicare, it’s because you’re eligible for Medicare (due to age or disability) and your income and assets are also low enough that you’ve either qualified for help covering some of the costs that Medicare beneficiaries incur, or qualified for full coverage under both Medicare and Medicaid, with Medicaid picking up the tab for Medicare premiums and out-of-pocket expenses and certain services that Medicare does not cover.

States have different income and asset limits for their different Medicaid programs – including limited Medicaid benefits that pay for Medicare’s premiums and/or cost-sharing (Medicare Savings Programs). Because these standards vary, you should contact resources in your state to see which program(s) you might qualify for and for help applying. You can click on a state on this map to see specific details about Medicaid-funded assistance that’s available to eligible Medicare beneficiaries.

If you do have some sort of additional Medicaid coverage, you fall into one of two main categories of dual-eligibles:

“Full-benefit dual-eligibles” have Medicare and receive a full array of benefits under Medicaid.

If you’re a full-benefit dual-eligible, Medicare will be your primary source of coverage for medical services, with Medicaid helping pay Medicare premium costs and co-pays.

Medicaid also helps “full duals” by covering services that Medicare doesn’t cover, such as long-term care (explained later in this article).

A smaller segment of dual-eligibles – “partial duals” – qualifies to have Medicaid pay some but not all expenses, such as Medicare premiums and/or cost-sharing. So if you’re a “partial dual,” you would not be covered for Medicaid-only services; rather, you’d receive Medicaid’s help covering your Medicare premiums and your cost-sharing for Medicare-covered services.

Generally, “partial duals” have income and assets that may be low – but not low enough to qualify for full Medicaid benefits in their state.

You can find out if you may qualify for Medicaid by contacting your state’s Medicaid office. If you are applying for Medicaid, states usually have 45 days to process your application (but they have 90 days to do this if you’re disabled). This page, maintained by the Centers for Medicare and Medicaid Services, has contact information for the Medicaid offices in each state.

There are four different types of Medicare Savings Programs, and they have varying income requirements. In 2022, a single individual can qualify for an MSP with a monthly income as high as $1,469, although the limits for some of the MSPs are lower than that.

And the MSP that provides assistance to certain people who are disabled but still working has a much higher income limit (up to $4,379 per month for a single person in 2021). The MSPs in your state may also use an asset test – which is $7,970 for individuals and $11,960 for couples in most states.

Supplemental Security Income (SSI) enrollees are automatically eligible for full Medicaid in most states. Some of these states automatically enroll you in Medicaid if you have SSI – but other states require you to apply for it yourself. (You’ll usually qualify for Medicaid due to your financial circumstances if you’re poor enough to receive SSI benefits – even if you’re not automatically enrolled.)

However, this is not the case in every state. Connecticut, New Hampshire, Hawaii, North Dakota, Illinois, Oklahoma, Minnesota, Virginia and Missouri have eligibility limits (for income or resources) for Medicaid that are more restrictive than the SSI program.

Medicaid’s income rules for beneficiaries without SSI also vary from state to state, but are usually between 74% and 100% of the federal poverty level. (In 2021, those levels are equal to $794 and $1073 a month for individuals, respectively.)

As of 2018, there were 40 states where single Medicaid applicants needed to have less than $2,000 in savings to qualify for full Medicaid benefits, and couples couldn’t have more than $3,000.

Some states also allow you to qualify for Medicaid by making a “spend down” payment or submitting medical bills equalling a specific amount.

The income limit for Medicaid nursing home benefits and Home and Community Based Services (HCBS) waivers are usually somewhat higher. Most states also allow enrollees to qualify for these long-term care benefits with incomes up to 300% of the SSI payment amount (which equals $2,383 per month in 2021).

Coverage and benefits for dual-eligible beneficiaries vary widely – both because of each individual’s financial situation, but also often because of the state where the beneficiary resides.

States are required to cover certain services for Medicaid recipients, including skilled nursing facility or hospice services. But states can go above and beyond these “mandatory levels” to cover expenses such as long-term care services provided in your home.

For this reason, alone, it’s important to do your homework and get advice tailored to your specific situation.

The route to enrollment in both programs varies, but typically, dual-eligibles start out enrolled in Medicare, and then gain the additional coverage through Medicaid on the basis of income/assets or life circumstances (such as a severe disability). These dual-eligibles qualify because they or someone else realizes the beneficiary also needs Medicaid.

You could be enrolled in Medicare, for instance, and then be automatically also enrolled in Medicaid by a state agency, which might determine your Medicaid eligibility based on your enrollment in another program, such as the Supplemental Nutrition Assistance Program (SNAP) or Supplemental Security Income. (At some point, you may get a notification by mail that you’ve been enrolled in Medicaid.)

Another catalyst for Medicaid enrollment is often a skilled nursing facility or long-term care facility (commonly referred to as a nursing home). Because Medicare coverage in these facilities is generally limited to people who need “skilled care” in an institutional setting (such as rehabilitation from an injury or accident), these facilities may apply for Medicaid on behalf of patients who exhaust Medicare’s coverage.

Unless you also need skilled care, Medicare will never pay for custodial care – that is, help with daily activities that can be performed by an “unskilled” professional such as bathing or getting dressed. (Medicare may pay or provide limited help with these items while you are also receiving skilled care.)

Unlike Medicare, Medicaid can help pay for custodial care in a nursing facility or at home. Again, eligibility rules and the extent of your coverage can vary by state. But nationwide, six out of ten nursing home residents are covered by Medicaid.

More specifically, how might a beneficiary of one program also end up enrolled in both? The following are just a few hypothetical situations:

Yes. Some Medicare beneficiaries – especially low-income seniors – qualify for Medicaid assistance but don’t end up receiving it because they either don’t realize they qualify or they aren’t able to navigate the lengthy application and renewal processes.

If you’re not certain whether you qualify, you should contact your local Medicaid office or one of the resources listed at the end of this article.

If you were surprised to learn that Medicaid works hand in hand with Medicare, you might also be surprised to know that there’s a long list of government-sponsored private plans that provide coverage to dual-eligibles.

Sometimes your state will require you to enroll in one of these private plans; other times you’ll have the option to not enroll. In either case, your state and the federal government (Medicare) together pay most or all costs associated with your enrollment.

Unlike “regular” Medicare and Medicaid, privately administered plans can offer you additional benefits such as care coordination or case management. In some cases, these government-administered private insurers offer you a way to receive coverage under Medicare and Medicaid (including long-term or home care) through a single plan rather than several different ones. While the government may pay for the plan’s costs, the plan is run by a private insurer.

The plans vary a lot: Some cover a wide range of benefits – including all of your medical, hospital prescription drugs, and home or nursing care. Other plans only cover specific portions of your care, such as Medicaid’s home care benefits. The availability of these private plans also depends on the state where you live, meaning that some dual-eligibles have more plan options than others.

So how do dual-eligibles learn about and choose these private plans? There are several ways:

In addition to covering expenses that Medicare will not cover – such as long-term care – Medicaid can pay for your co-pays and deductibles for Medicare-covered services.

A plan may be privately administered, but if you have both Medicare and Medicaid, you may not have to pay more for this coverage than you did before you enrolled. This is because the government pays for most or all of your coverage. (You also may not have a choice but to enroll, depending on the type of plan and your state’s own rules. Follow the information in this article to ensure you choose a plan that fits your needs. It might even save you money.)

Often, a privately administered dual plan can save you money by covering expenses that regular Medicare doesn’t cover (for example, over-the-counter drugs or additional benefits for hearing aids). That said, regular state-run Medicaid can also offer these types of benefits.

Many states contract with private companies to provide Medicaid and dual-eligible plans – and most of the time, the plan’s premium costs are completely paid for on your behalf. But be sure to ask about costs before enrolling in any private health plan.

Just like with any other health insurance coverage, the plans you choose for your coverage as a dual-eligible will impact and potentially limit or improve your healthcare experience – including your choice of healthcare providers, whether you need to ask permission before seeing a specialist, or how you receive your home care.

Because there’s so much variation in plans geared toward dual-eligibles, it behooves you to do your homework – and that will include seeking help from experts who can analyze your particular situation and give you advice tailored to your needs. Among the resources available to you:

1-800-MEDICARE call center representatives also have access to enrollment information, resources available in your state, and can help with some Medicare-related enrollment changes. These reps will be able to tell you what Medicare or duals private plan you have, but they can’t make changes or recommendations regarding MLTSS coverage (which is a Medicaid-only service).

Legal aid societies and similar organizations, many of which operate healthcare hotlines to assist with coverage questions. Trained attorneys and advocates can give specific advice tailored to what’s happening in your state. They can also discuss income, assets, eligibility and other important issues.

If you call your Legal Aid or SHIP, you can begin your conversation by stating that you’re looking for help with Medicare’s costs and/or long-term care. You can ask to talk with someone to help you determine whether Medicaid or a Medicare Savings Program could save you money or offer additional benefits.

State Health Insurance Assistance Programs (SHIPs) are Medicare counseling services in each state. These trained counselors should be able to refer you to local resources on Medicaid benefits if they can’t answer your specific questions themselves. You can find your state SHIP here, and our state guide to Medicare includes SHIP listings within each state overview.

Private insurance brokers may specialize in Medicare private plans, some of which are tailored to the needs of dual-eligibles. Be careful, though, to work with your insurance broker to consider all available Medicare plans so you pick the one that meets your coverage needs – and saves you the most money.

Enrollment brokers are state-contracted call centers that facilitate enrollment in the various plans that cover recipients of both Medicaid and Medicare. This hotline is typically the only one where customer service representatives (CSRs) can make enrollment changes for you. You can search online for your state’s hotline, but also make sure to check with the appropriate legal aid society’s healthcare group for unbiased advice.

Your state’s call center (which will have a different name in your state) or Medicaid office may have answers to more basic questions (such as whether you have Medicaid or which plan you have).

Family or estate planning attorneys can answer questions about qualifying for Medicaid based on your assets and/or income. They may be able to help you plan for your healthcare needs using a Special Needs Trust. You can find a legal referral in the elder law section of your state bar association’s website.

There are no federal rules guaranteeing access to Medigap plans for enrollees under age 65, but states can create their own rules to ensure that disabled Medicare beneficiaries are able to enroll in supplemental coverage.

Americans who are enrolled in both Medicaid and Medicare are called dual-eligible beneficiaries, or Medicare dual eligibles or sometimes simply duals.

People with Medicare and Medicaid are known as dual eligibles – and account for about 20 percent of Medicare beneficiaries (12.1 million people). Learn how that status affects your coverage.

There are three main ways for lower-income Medicare beneficiaries to cover out of-pocket-costs when they can't afford to purchase a Medigap supplemental plan or a Medicare Advantage policy.

If your income is high or very low – or you're feeling lucky – you might be able to rely on traditional Medicare. Here's why most people don't.

There are no federal rules guaranteeing access to Medigap plans for enrollees under age 65, but states can create their own rules to ensure that disabled Medicare beneficiaries are able to enroll in supplemental coverage.

Americans who are enrolled in both Medicaid and Medicare are called dual-eligible beneficiaries, or Medicare dual eligibles or sometimes simply duals.

People with Medicare and Medicaid are known as dual eligibles – and account for about 20 percent of Medicare beneficiaries (12.1 million people). Learn how that status affects your coverage.

There are three main ways for lower-income Medicare beneficiaries to cover out of-pocket-costs when they can't afford to purchase a Medigap supplemental plan or a Medicare Advantage policy.

If your income is high or very low – or you're feeling lucky – you might be able to rely on traditional Medicare. Here's why most people don't.