You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

A recent Kaiser Family Foundation analysis found that the vast majority of Medicare beneficiaries – about nine out of ten – do not change their Part D prescription coverage from one year to the next. But we wondered how many of those beneficiaries are regularly comparing their options and deciding to keep their current plan – as opposed to just letting their coverage renew without comparing options.

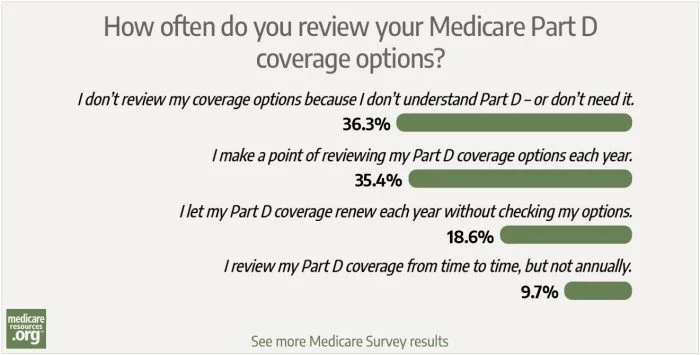

So in our most recent survey we asked how often our readers review their Medicare Part D coverage. Here’s how the results stacked up, with the percentage of respondents who selected each option:

We knew going into the survey that nearly 77% of all Medicare beneficiaries have Part D coverage, split almost equally between stand-alone Part D plans and Medicare Advantage plans with integrated Part D coverage. In other words, almost a quarter of all Medicare beneficiaries are not enrolled in Part D. Many of these individuals have creditable drug coverage from a current or former employer or spouse’s employer, although some simply do not have any drug coverage at all.

So it’s not surprising that our largest response category encompassed people who don’t understand Part D or just don’t need the coverage, given that nearly a quarter of Medicare beneficiaries aren’t enrolled in Part D.

But it’s important to understand that there’s a big difference between not needing Part D because you have other creditable coverage, versus “not needing” Part D because you don’t take any prescriptions.

If it’s the latter, you might find yourself in a tough situation if and when you eventually need expensive prescriptions. You’ll only be able to sign up for coverage during the fall enrollment period (October 15 to December 7, with coverage effective January 1) and you’ll also have to pay a late enrollment penalty for as long as you have Part D – likely the rest of your life.

It’s heartening to see that more than a third of our respondents review their Part D coverage annually. Although the KFF data indicate that only about one out of ten beneficiaries make changes to their coverage, a larger percentage of our respondents are actively reviewing their plans each year.

Keeping your current plan may well be the best option, and as long as you’re comparing plans annually, you won’t be inadvertently missing out on a plan that might provide a better overall value.

But 19% of our respondents are enrolled in Part D coverage and simply let it renew each year, without checking to see if there are better options available. This is not a good strategy, even if you’re certain that the plan you have was the best option when you enrolled in it.

Part D plans – including the Part D coverage that’s integrated with most Medicare Advantage plans – can change significantly from one year to the next. Insurers can change their formularies (covered drug lists), move drugs from one tier to another (which changes out-of-pocket costs), and make changes to their list of participating pharmacies.

In some cases, plans are discontinued and members are automatically moved to a replacement plan unless they actively shop for new coverage during the annual election period. Even if very little about your plan is changing, premiums vary from one year to another, and your specific prescription needs can also change over time.

All of this means that if you’re not actively comparing your Part D options during the annual election period, there’s a good chance you’re leaving money on the table. You might be paying too much in premiums, or missing out on a plan that would cut your out-of-pocket costs at the pharmacy.

The other 10% of our respondents are comparing their coverage options on a somewhat regular basis, but not annually. This is better than letting a plan auto-renew for years on end, but an annual review is a better approach, given that Part D benefits and premiums change every year.

There are multiple stand-alone Part D plans available everywhere in the U.S., and Medicare Advantage plans available in nearly all parts of the U.S. So Medicare beneficiaries have a plethora of prescription options from which to choose. (If you’re trying to decide between Medicare Advantage versus Original Medicare with supplemental Medigap and Part D, read our summary of points to keep in mind).

The annual enrollment window starts in under two months, on October 15. If you’re not in the habit of reviewing your Part D coverage each year, now’s a good time to make a plan to do so during the upcoming enrollment window.

You can use Medicare’s Plan Finder tool to see how each of the available options would cover the specific drugs you need. And you can also see how your costs would vary on each plan depending on the pharmacy you use. This is your opportunity to see if there are any available plans that would reduce your total costs, including premiums as well as out-of-pocket costs at the pharmacy.

If you’re struggling to understand how prescription drug coverage works, a Medicare insurance broker can help you make sense of it all. (You can talk with a licensed Medicare agent by calling the number at the top of this page.)

The State Health Insurance Assistance Program (SHIP) in your state can provide Medicare counseling and enrollment assistance if you need it. Medicare’s website also has some helpful tips for choosing a Part D plan.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org. Her state health exchange updates are regularly cited by media who cover health reform and by other health insurance experts.