You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Yes. The best time to enroll is during your Medigap open enrollment period, a six-month window of time that begins on the first day of the month that you are at least 65 years old and are enrolled in Medicare Part B1 (you must also be enrolled in Part A to buy a Medigap plan, but for people who enroll in Part A when they turn 65 but delay their enrollment in Part B, the Medigap open enrollment period begins once they enroll in Part B).

During this period, a private insurance company that offers Medigap coverage can not:

Even if you enroll during your initial enrollment period, a private Medigap insurer may refuse (for up to six months) to pay your out-of-pocket expenses for a pre-existing health issue. If your pre-existing condition was diagnosed or treated within six months before the date your Medigap supplemental coverage was to begin, the insurance company can make you wait up to six months before covering your out-of-pocket expenses for the pre-existing condition.

But if you had creditable coverage before enrolling in Medigap, without a gap in coverage of more than 63 days, the pre-existing condition waiting period will be reduced by the number of months that you had creditable coverage.2 So if you had continuous coverage for six or more months before enrolling in Medigap, you won’t have a pre-existing condition waiting period. The rules can be confusing, so don’t hesitate to talk to a representative of the Medigap insurance company for clarification.

After your six-month open enrollment window, Medigap plans are medically underwritten in nearly every state, meaning that if you apply for coverage outside of your open enrollment window, you can be declined or charged more based on your medical history.

There are also some limited special enrollment periods for Medigap coverage, including

You can certainly apply for a new Medigap plan during the annual Medicare open enrollment period (October 15 to December 7). But that window is no different from any other time of the year when it comes to Medigap.

The annual Medicare open enrollment period (annual election period) is for Medicare Advantage and Part D plans, but it doesn’t change anything about the normal enrollment rules for Medigap. In most states, if your initial enrollment window has ended and you don’t qualify for a special enrollment period, Medigap insurers will use medical underwriting if you submit an application for a new plan, regardless of what time of year you apply.

So for example, if you want to use the annual open enrollment period to switch from Medicare Advantage to Original Medicare, you can do that. And you’ll be able to enroll in a stand-alone Part D plan to supplement your Original Medicare. You’ll be able to apply for a Medigap plan as well, but in most states, the coverage will not be guaranteed issue — your eligibility will depend on your medical history. (Note that if your Medicare Advantage plan is ending on Dec. 31 and thus not available for renewal, you will have guaranteed-issue access to most of the Medigap plans available in your area, if you choose to switch to Original Medicare instead of a different Medicare Advantage plan.1)

The same will be true if you want to try to switch from one Medigap plan to another. Let’s say you have Original Medicare plus a Part D plan and Medigap plan, and you want to make changes to your coverage. You can switch to any available Part D plan during the annual open enrollment period, and your medical history will not be a factor. But in most states, your medical history will be a factor if you submit an application for a different Medigap plan.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written hundreds of opinions and educational pieces about the Affordable Care Act and Medicare for healthinsurance.org and medicareresources.org.

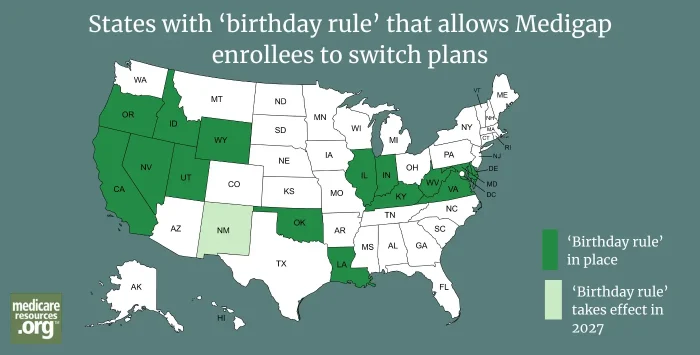

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

Modern Medigap plans do not include prescription drug benefits. Instead, Medicare offers prescription drug coverage under Part D. Medicare enrollees can get prescription coverage either by switching to a Medicare Advantage plan or by purchasing a stand-alone Medicare Part D plan (PDP) to go along with Original Medicare.

Can't wait to make changes to your Medicare coverage during open enrollment? Just know that open enrollment can also be an occasion for major enrollment blunders. Here are three that you'll want to steer clear of.

Learn how and when to enroll in Original Medicare, Medicare Advantage, Medigap, and Part D coverage. Get plan information and a free quote today.

Even after Open Enrollment has ended, some people may find that they can enroll in Medicare or make changes to their coverage due to their circumstances or a qualifying life event.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

Considering a change to your Medicare coverage? Consider these 10 factors when choosing between Medicare Advantage, Medigap, and Part D coverage.

Medigap plan changes are limited, but 11 states offer Medigap enrollees special enrollment – and five do it with a 'birthday rule.'

Modern Medigap plans do not include prescription drug benefits. Instead, Medicare offers prescription drug coverage under Part D. Medicare enrollees can get prescription coverage either by switching to a Medicare Advantage plan or by purchasing a stand-alone Medicare Part D plan (PDP) to go along with Original Medicare.

Can't wait to make changes to your Medicare coverage during open enrollment? Just know that open enrollment can also be an occasion for major enrollment blunders. Here are three that you'll want to steer clear of.

Learn how and when to enroll in Original Medicare, Medicare Advantage, Medigap, and Part D coverage. Get plan information and a free quote today.

Even after Open Enrollment has ended, some people may find that they can enroll in Medicare or make changes to their coverage due to their circumstances or a qualifying life event.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

Considering a change to your Medicare coverage? Consider these 10 factors when choosing between Medicare Advantage, Medigap, and Part D coverage.

Footnotes