You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

Generally, a prescription written by your doctor will be covered under your drug plan if you follow these requirements:

Medicare has a plan finder tool where you can enter your medications and see how much your out-of-pocket costs will be for each of the plans available in your area. If you’re currently taking medications, using this tool during open enrollment is essential.

Drug formularies change from one year to the next, and different Medicare Part D plans offer different levels of coverage for different drugs. So it’s important to shop around during open enrollment (October 15 to December 7) to make sure you’re enrolling in the plan that will provide you with the best coverage for the coming year.

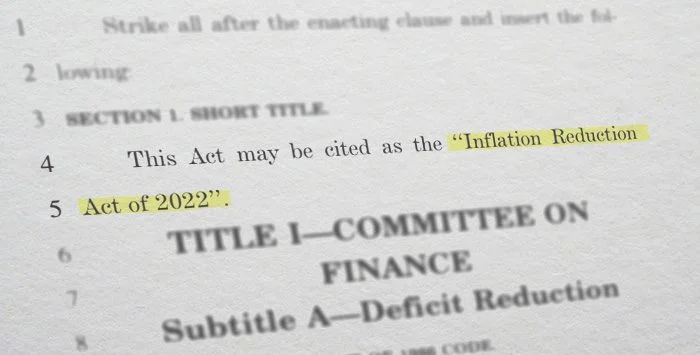

There have been some important improvements to Medicare Part D in recent years, as a result of the Inflation Reduction Act. These include $35 insulin, free recommended vaccines, the elimination of cost-sharing in the catastrophic coverage level, and a $2,000 cap on out-of-pocket costs as of 2025 (increasing to $2,100 in 2026).1

But that cap only applies to drugs that are covered by a given plan. So it’s still important for enrollees to actively compare their plan options each fall, to make sure that the plan they have for the coming year will cover the specific medications they take.

If you’re not taking medications, you still need to enroll in a Part D plan as soon as you become eligible for Medicare (unless you have creditable drug coverage from a plan offered by your employer or your spouse’s employer, or a retiree drug plan). But people in this situation often just pick the cheapest plan available. If you skip Part D altogether because you’re not taking any medications, you could end up paying a lot more in the long run, due to lack of coverage as well as the late enrollment penalty.

A person who skips Part D coverage and then ends up being prescribed expensive medication mid-year will be unable to enroll in a Part D plan until the next open enrollment period, with coverage effective the following January. And for every month that you were eligible to enroll in Part D but didn’t (and didn’t have creditable drug coverage from another source), you’ll pay a surcharge equal to 1% of the national base beneficiary Part D premium — on top of your regular Part D premium.2

So if you wait three years to sign up for Part D coverage because you weren’t taking medications during those three years, you’ll pay the regular Part D premium for the plan you pick, plus a surcharge equal to 36% of the national base beneficiary premium. That surcharge will continue for as long as you have Part D, and will increase over time as the national base beneficiary premium increases.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written hundreds of opinions and educational pieces about the Affordable Care Act and Medicare for healthinsurance.org and medicareresources.org.

Beginning in 2023, a series of changes began to be phased in under the Inflation Reduction Act, designed to lower out-of-pocket costs, expand access to vaccines, and rein in drug price increases.

We asked how confident our readers were with comparison shopping for a Medicare Part D plan during the 2022 Medicare Annual Enrollment Period. Here's what we learned from more than 350 survey responses.

Medicare beneficiaries can call an easy-to-remember toll-free number – 1-800-MEDICARE – for information that includes specific billing questions and questions about claims.

Reasons to consider a change to your Medicare prescription drug coverage may include high premiums, changes to your prescriptions or your plan's formulary, and your access to in-network pharmacies.

Prescription drugs – and drug coverage – can be less expensive if you're willing to do a little research and to reach out for help. Here are eight strategies that will empower you to take control of your drug coverage and your medication costs.

If you're enrolled in a Medicare Advantage plan and you're not happy with it, you can switch plans during Medicare's annual open enrollment period. Here are four reasons why you might change coverage.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

Beginning in 2023, a series of changes began to be phased in under the Inflation Reduction Act, designed to lower out-of-pocket costs, expand access to vaccines, and rein in drug price increases.

We asked how confident our readers were with comparison shopping for a Medicare Part D plan during the 2022 Medicare Annual Enrollment Period. Here's what we learned from more than 350 survey responses.

Medicare beneficiaries can call an easy-to-remember toll-free number – 1-800-MEDICARE – for information that includes specific billing questions and questions about claims.

Reasons to consider a change to your Medicare prescription drug coverage may include high premiums, changes to your prescriptions or your plan's formulary, and your access to in-network pharmacies.

Prescription drugs – and drug coverage – can be less expensive if you're willing to do a little research and to reach out for help. Here are eight strategies that will empower you to take control of your drug coverage and your medication costs.

If you're enrolled in a Medicare Advantage plan and you're not happy with it, you can switch plans during Medicare's annual open enrollment period. Here are four reasons why you might change coverage.

Enrollment dates for Medicare are critical. Missing an enrollment date could cost you higher premiums down the line — or it could cost you coverage entirely.

Footnotes