You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

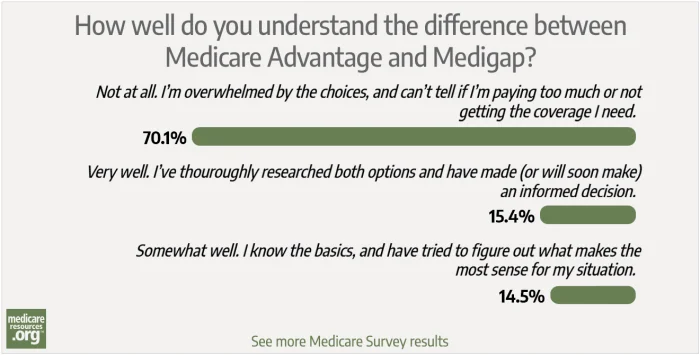

EDITOR’S NOTE: Our Medicare Surveys “take the pulse” of our audience – assessing our readers’ experiences with Medicare and their attitudes toward the program. The questions and the results are not intended to be scientific.

Confused by the differences between Medigap (Medicare supplement insurance) and Medicare Advantage? You’re certainly not alone. More than two-thirds of the respondents in our most recent survey indicated that they don’t understand the differences and are overwhelmed by the available choices – and dozens of readers commented about their experiences on Facebook.

More than 200 of our readers answered our question about how well they understand the differences between Medigap and Medicare Advantage:

The confusion and sense of being overwhelmed are understandable: Although plan availability varies from one area to another, the average Medicare beneficiary can choose from among 33 Medicare Advantage plans and dozens of Medigap plans.

Most beneficiaries are deluged by advertising each fall, particularly for Medicare Advantage plans. But the marketing materials are designed to play up each plan’s strengths, and generally don’t help beneficiaries understand whether Medigap or Medicare Advantage will best fit their needs.

If you’d like to dig a little deeper, we’ve got detailed resources explaining both Medigap and Medicare Advantage, as well as ten points to keep in mind when you’re deciding between them.

But here are some basics to get you started:

Both Medigap and Medicare Advantage are offered by private insurance companies. Medigap is used in conjunction with Original Medicare (Parts A and B), whereas Medicare Advantage wraps all of the Medicare Part A and Part B benefits into one plan. And most Medicare Advantage plans will generally also include extras like dental and vision coverage, hearing aid coverage, and gym memberships.

If you enroll in Original Medicare plus a Medigap plan, you’ll have access to most doctors and hospitals nationwide. (Here’s more about how medical providers work with Medicare).

With Medicare Advantage, on the other hand, you’ll need to pay attention to the insurer’s provider network and rules. (If it’s an HMO, for example, you’ll need to stay within the provider network for most medical services.)

Most Medicare Advantage plans include Part D prescription coverage, whereas you’ll need to purchase a separate stand-alone Part D plan if you go with Original Medicare plus Medigap.

Medigap plans are standardized in the same way in all but three states, making it fairly easy to compare plans. But prices will vary from one company to another, as will the way they adjust pricing over time.

Medigap premiums vary tremendously depending on where you live and the plan you select, but they tend to be higher than Medicare Advantage premiums. More than half of all Medicare Advantage plans have no premium at all other than the premium for Medicare Part B (which is paid in addition to whatever the Medicare Advantage plan charges).

Medigap plans are designed to cover the out-of-pocket costs (deductibles and coinsurance) that go along with Original Medicare. With just a few exceptions, Medigap plans will not pay for expenses that aren’t covered at all by Medicare (routine dental/vision services, custodial long-term care services, etc.).

Each standardized Medigap plan design covers certain out-of-pocket costs, so you’ll want to pay attention to how those work and understand which costs you’ll have to pay yourself with each plan (if you’re new to Medicare, you’ll have to pay at least the Part B deductible yourself, but there are Medigap plans available that will pick up the rest of your potential out-of-pocket costs).

With a Medicare Advantage plan, your out-of-pocket expenses will vary from one plan to another, but are capped at no more than $7,550 in 2021. (Note that this does not include out-of-pocket costs for prescriptions, which are counted separately as part of the plan’s Part D coverage).

Original Medicare + Medigap + Part D will tend to provide more robust coverage than a Medicare Advantage plan, meaning that your out-of-pocket costs will likely be lower if and when you need medical care, and you’ll have access to more medical providers.

But your total premiums are also likely to be higher with Medigap, so there’s no one-size-fits-all. (If premiums are a sticking point but you’d like the broader provider network that comes with Original Medicare plus a Medigap plan, consider Medigap Plan K, L, or the high-deductible version of Plan G. Their premiums will be lower to account for the fact that you’ll have higher — but still fairly manageable — out-of-pocket costs than you’d have with other Medigap plans.)

Medicare Advantage coverage can be changed during the fall election period (commonly known as Medicare open enrollment) or the Medicare Advantage open enrollment period at the start of each year. But there is no annual enrollment period for Medigap, unless you’re in one of the handful of states with extended access to Medigap plans.

In the rest of the country, in most circumstances, insurers can take your medical history into account if you apply for a Medigap plan after your initial six-month enrollment period ends.

This is an important point to keep in mind. If you pick a Medigap plan, you’ll want to consider not only your current medical needs, but what your needs might be many years in the future. And understand that if you start out with Medicare Advantage due to the lower premiums, your ability to switch to Medigap in the future might be limited, depending on your health.

If you’re feeling overwhelmed and confused by the Medicare options available to you, help is available. You can reach out to the State Health Insurance Assistance Program (SHIP) in your state, or a trusted broker who can help you pick a plan. (You can call the number at the top of this page to talk with a licensed professional about your Medicare coverage options.)

And be sure to reevaluate your choice each year. If you’re enrolled in Medigap, you’ll want to double check each year to make sure that your Part D plan is still the best option to meet your prescription needs. You can use Medicare’s plan finder tool to see how each available plan will work for your specific drugs and pharmacy options. If a different Part D plan will better suit your needs, you can switch plans during the fall enrollment window.

And if you’re enrolled in Medicare Advantage, you’ll also want to do an annual comparison to see if a different plan might better fit your needs for the coming year (consider medical provider networks and out-of-pocket costs, as well as how the available plans will cover your prescriptions).

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org. Her state health exchange updates are regularly cited by media who cover health reform and by other health insurance experts.