You're on your way!

You're being directed to a third-party site to get a quote.

Since 2011, we've helped more than 5 million visitors understand Medicare coverage.

By shopping with third-party insurance agencies, you may be contacted by a licensed insurance agent from an independent agency that is not connected with or endorsed by the federal Medicare program.

These agents/agencies may not offer every plan available in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all options available.

EDITOR’S NOTE: Our Medicare Surveys “take the pulse” of our audience – assessing our readers’ experiences with Medicare and their attitudes toward the program. The questions and the results are not intended to be scientific.

Entry to the Medicare system means Americans receive comprehensive coverage and a large selection of healthcare providers – and enrollment is typically greeted with relief. After years of paying Medicare taxes, Americans often are eager to receive their Medicare benefits – leaving the uncertainties of employer-sponsored or individual health coverage behind.

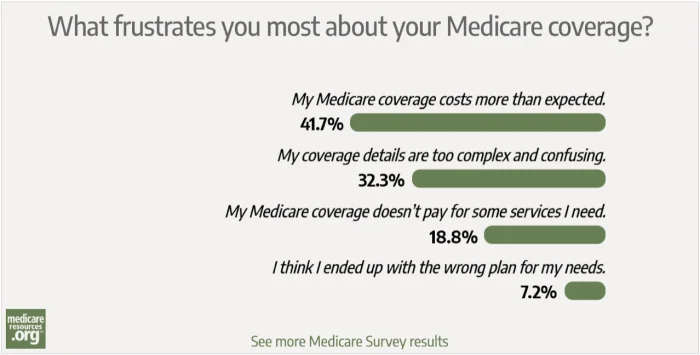

But – like other forms of health coverage – Medicare can be a source of frustration and confusion for enrollees. We wanted to explore those frustrations in our most recent poll of our site’s readers. In the survey – conducted over the past 2 1/2 weeks – we asked, “What frustrates you most about your Medicare coverage?”

The responses:

The top frustration identified by this poll is unexpected costs of Medicare coverage – and there are a couple of fairly obvious explanations.

The first is that enrollees are simply going into Medicare with an expectation that their new safety net isn’t going to cost much. Based on my experience working with enrollees, I know that many enrollees are simply surprised to learn that Medicare has significant premiums and out-of-pocket costs.

While Medicare Part A is, in fact, premium-free for most enrollees, Part B usually costs $144.60 a month (increasing to $148.50 a month in 2021). And monthly premiums for Part D average $42 in 2020. Total Medicare premiums? They can exceed $350 each month when the cost of Medigap – which covers out-of-pocket expenses under Parts A and B – is added into the equation.

But premiums are only part of what Medicare enrollees pay for healthcare. Medicare beneficiaries who enroll in Medicare Advantage plans have to pay up to $6,700 in cost sharing annually before the plan will cover the full cost of their medical services (this upper limit is increasing to $7,550 in 2021, although many plans have lower out-of-pocket caps). And that doesn’t count the cost of prescription drugs on Medicare Advantage plans that have integrated Part D coverage.

The Medicare Part D benefit also has significant cost-sharing. Part D enrollees pay a large percentage of the cost for medications until they reach “catastrophic coverage” (i.e., when the plan and enrollee have spent $6,350 together; this threshold is increasing to $6,550 in 2021; note that the amount the drug plan pays while the enrollee is in the donut hole does not count towards that threshold). Enrollees then pay a small co-pay or 5 percent of the cost for their medications – whichever is greater – after reaching this part of the Part D benefit.

But another explanation is that many of our readers who were frustrated by unexpected costs are getting by with limited incomes. In 2016, half of all Medicare beneficiaries had annual incomes below $26,200 – and one-quarter had incomes below $15,250. Medicare beneficiaries’ incomes decline with their age – and half of beneficiaries age 85 or older had annual incomes below $20,400 in 2016.

The good news is that some respondents who struggle with Medicare’s expenses may be eligible for help with their Medicare Part B premiums through a Medicare Savings Program (MSP) – or prescription drug assistance through the Extra Help benefit.

MSPs pay for Part B premiums – and sometimes also pay for Medicare Part A premiums and Part A and B cost-sharing. The upper income limit for MSPs is $1,456 per month for singles and $1,960 per month for couples. (Many states also have an asset limit for MSPs.)

Recipients of the MSP automatically receive Extra Help – a federal program that dramatically lowers prescription drug expenses under Part D. Lower-income enrollees can also apply for Extra Help directly – and may qualify with monthly incomes up to $1,615 for individuals and $2,175 for spouses. Extra Help applicants also have to meet an asset limit.

Beneficiaries with slightly higher incomes than this may qualify for help through a State Pharmaceutical Assistance Program (SPAP). SPAPs usually offer assistance with Part D expenses for enrollees with low- to moderate incomes – although in some states help is limited to those with specific medical conditions. Medicare beneficiaries can also save on premiums by switching to a lower-cost Medigap or Medicare Advantage plan – although this could increase their out-of-pocket expenses.

After unexpected costs, the top frustration for our readers is complex and confusing coverage details.

It’s no secret that Medicare is complicated. Beneficiaries have to navigate among Parts A, B, C, and D – along with the potential choice of a Medigap plan. They then have to actually use their health coverage – which requires deciphering complicated coverage rules, navigating provider networks and insurance formularies, and using a participating pharmacy.

The good news for these beneficiaries is that there are actually great sources of information – available for free – that can help enrollees more clearly understand important aspects of their Medicare coverage. Among these resources: representatives at 1-800-MEDICARE, State Health Insurance Assistance Program (SHIP) counselors, and Medicare brokers.

It’s worth mentioning that this website – medicareresources.org – is rich with information dedicated to helping enrollees understand their plan options, eligibility and enrollment guidelines and reviewing details about benefits such as vision and dental. Got a question? It’s probably been addressed in our Frequently Asked Questions section.

Along with costs, it’s also obvious that many of our readers – 18 percent of those who responded – feel that Medicare benefits don’t cover services they need, such as dental or vision care or exercise memberships. I am surprised more readers didn’t select this response.

Original Medicare doesn’t include a dental benefit, although some Medicare Advantage plans offer limited dental and vision coverage. A 2012 survey of Medicare beneficiaries found that high-income Medicare beneficiaries – who can pay out-of-pocket for dental care – were three times as likely to have received dental care in the prior 12 months than low-income beneficiaries. That survey highlighted the need to add a dental benefit to Medicare, so no beneficiaries have to pay for dental care out-of-pocket.

Medicare beneficiaries can purchase stand-alone dental coverage for an additional monthly premium. But stand-alone dental plans usually have waiting periods for expensive care (such as bridges, crowns, and root canals).

Medicare also doesn’t cover routine vision care – although it does cover medical services for beneficiaries who have health conditions that affect their eyes and vision. And, while stand-alone vision plans exist, they aren’t commonly used by Medicare beneficiaries. (Some Medicare beneficiaries receive coverage for dental and vision services through Medicaid.)

Another additional benefit some Advantage plans offer is an exercise membership. Although these benefits (e.g., Silver Sneakers) are nice to receive as part of one’s health plan, Medicare beneficiaries shouldn’t base their decision to enroll in a plan on an exercise membership alone. Other factors – such as premiums, provider networks, and cost-sharing – should factor into the decision to purchase a health plan.

Finally, another 6 percent of readers said they ended up in the wrong Medicare plan for their needs. This underscores how urgent it is that beneficiaries shop around – comparing plans and benefits either online or by calling a licensed Medicare agent for a thorough discussion of one’s budget and anticipated healthcare needs.

You can shop around during Medicare Open Enrollment each fall. Open enrollment ended December 7, but extended open enrollment is available in a dozen states thanks a special enrollment period for areas affected by disasters in 2020. And Medicare beneficiaries who are already enrolled in Medicare Advantage can make a plan change during Medicare Advantage Open Enrollment (from January 1 through March 31), by either switching to a different Medicare Advantage plan or moving to Original Medicare.

The bottom line here is that Medicare can be a whole lot less frustrating for enrollees when they do their homework. That means taking the time before enrolling to get a better sense of Medicare’s coverage and its costs – and seeking advice and counsel from the aforementioned resources.

Josh Schultz has a strong background in Medicare and the Affordable Care Act. He coordinated a Medicare assistance contract at the Medicare Rights Center in New York City. Josh also helped implement health insurance exchanges at the technology firm hCentive. He has also held consulting roles, including at Sachs Policy Group, where he worked on Medicare and Medicaid issues.