EDITOR’S NOTE: Our Medicare Surveys “take the pulse” of our audience – assessing our readers’ experiences with Medicare and their attitudes toward the program. The questions and the results are not intended to be scientific.

Medicare is a single-payer program run by the federal government and available nationwide, but the amount that Medicare’s 63 million beneficiaries pay in monthly premiums varies considerably from one person to another.

Although Medicare coverage is heavily subsidized by the federal government via payroll taxes and general revenues, most beneficiaries also have to pay premiums for their coverage. But the amount that they pay depends on their income and assets, where they live, the Medicare coverage options they choose, and whether they have access to an employer-sponsored plan to supplement their Medicare coverage.

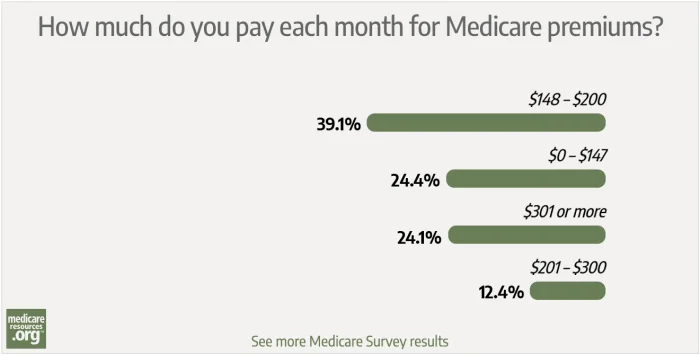

To get an idea of how much people are paying, we asked our readers with Medicare coverage to tell us how much they pay each month in total premiums, including any supplemental or additional coverage they might have. More than 330 people responded:

- 39.1% said they pay between $148 and $200 per month

- 24.4% said they pay between $0 and $147 per month

- 24.1% said they pay at least $301 per month

- 12.4% said they pay between $201 and $300 per month

Explaining the premiums paid by our respondents

Nearly two-thirds of our respondents are paying $200 or less in premiums each month, while nearly a quarter are spending more than $300 per month. Let’s take a look at how people might end up in each of the various premium categories.

Medicare Part B has a standard premium of $148.50 per month in 2021. Nearly all Medicare beneficiaries have to pay this premium (in most cases, it’s simply deducted from a beneficiary’s Social Security check), regardless of whether they’re enrolled in Original Medicare or Medicare Advantage. So it’s not surprising that three-quarters of our respondents are paying at least $148 per month in premiums.

Less than $148 a month in Medicare premiums

But how are the remaining quarter spending less than $148/month in premiums? There are a few ways this could happen:

- Beneficiaries who qualify for financial assistance with their Part B premiums via Medicare Savings Programs. (These programs are administered by state Medicaid offices, so there’s some state-to-state variation in terms of the income and asset limits.)

- Beneficiaries whose employers reimburse some or all of their Medicare premiums using a health reimbursement arrangement (HRA).

- Beneficiaries enrolled in Medicare Advantage plans that offer “giveback rebates,” which cover a portion of the Part B premiums that the enrollee would otherwise have to pay.

- Medicare beneficiaries who pay less than the standard amount for Part B due to the “hold harmless” provision that ensures Social Security checks don’t decline from one year to the next. People who have been receiving Social Security benefits for several years could still be paying less than the standard amount due to this rule.

Paying $148-$200 a month in Medicare premium

How about the 39 percent of respondents who are paying between $148 and $200 per month in premiums? This category covers a wide range of people, including:

- People who just have Original Medicare, and are only paying the Part B premium. (More than 6 million Medicare beneficiaries had only Original Medicare as of 2016, with no additional coverage).

- People who have Original Medicare plus a Part D prescription drug plan and/or a low-cost Medigap plan. There are Part D plans with premiums of less than $8/month in 2021. And depending on the state, some Medigap plans (particularly Plan K, Plan L, and the high-deductible versions of Plan F and Plan G) can be under $50/month. So it’s possible to have some supplemental coverage for Original Medicare and still have a total premium that comes in under $200/month, including the cost of Medicare Part B.

- Most Medicare Advantage enrollees. There are about 25 million people enrolled in Medicare Advantage plans, accounting for about 40 percent of all Medicare beneficiaries. More than half of these enrollees pay no premiums other than the Part B premium, although the average Medicare Advantage premium is $21/month in 2021. That’s in addition to the $148.50/month that beneficiaries pay for Medicare Part B, but the total premium cost for the average Medicare Advantage enrollee is between $148 and $200/month.

- Medicare beneficiaries who have employer-sponsored coverage that’s heavily subsidized by the employer. This can be in the form of active employee coverage or retiree coverage. If the employer is paying the bulk of the premiums, it’s possible that the enrollee’s total premiums, for Medicare Part B plus the employer-sponsored coverage, is under $200/month. People with active employee coverage generally only enroll in Part B if their employer has fewer than 20 employees, making the employer-sponsored coverage secondary to Medicare. If the employer has 20+ employees, the employee has likely delayed enrollment in Part B and their only premium is the cost of the employer-sponsored plan. But people with retiree coverage need to have both Part A and Part B, so their total premium cost will include the premiums for both Part B and the retiree coverage.

Paying $201 or more per month

And what about the nearly 37 percent of our respondents who are paying $201 or more per month (including the 24 percent who pay $301 or more)? This includes several categories of beneficiaries as well:

- Original Medicare beneficiaries who select higher-cost Part D and/or Medigap plans. Some Part D plans can cost well over $100/month. (But if your Part D plan has been getting increasingly expensive, you’ll want to make sure that you’re reviewing your coverage annually rather than just letting it auto-renew – you may find that you can get solid coverage for all of your medications with a much lower monthly premium. There’s an annual opportunity, from October 15 to December 7, during which you can switch you plan.) And depending on the state and the beneficiary’s age, there are plenty of Medigap plans with premiums well in excess of $150/month. The most popular Medigap plans tend to be the most comprehensive (Plan G, as well as Plan F for people who were already eligible for Medicare prior to 2020), and these also tend to be the most expensive. But the tradeoff is that enrollees with these Medigap plans have little or no out-of-pocket costs for Medicare-covered services.

- Original Medicare beneficiaries who are under 65 and charged higher premiums for Medigap coverage. (The rules on this vary considerably from one state to another.)

- Medicare Advantage enrollees with higher-cost plans. As of 2020, nearly one in five Medicare Advantage enrollees paid at least $50/month for their coverage, in addition to the cost of Part B. And 6 percent were paying at least $100 per month in addition to the cost of Part B. There may be a good reason to be paying this much – perhaps the plan you’ve picked has a better network that allows you access to the doctors and hospitals you need, or provides additional benefits that make the premiums worth it to you. But it’s important to make sure you’re reviewing your plan each year during open enrollment to make sure that you’ve still got the best option for your needs (you can do this from October 15 to December 7, or during the Medicare Advantage open enrollment period that runs from January through March each year). Repeatedly letting your coverage auto-renew might mean that you end up with premiums that are much higher than they’d be if you switched to a more competitive option.

- Beneficiaries with higher-cost employer-sponsored coverage. It’s quite common for a Medicare beneficiary with employer-sponsored retiree coverage to be paying well over $300/month in total premiums, including the cost of Part B and the employer-sponsored retiree plan. Active employees at small businesses (fewer than 20 employees) also need Part B, as their employer-sponsored coverage is secondary to Medicare, and the total premiums can be well over $300/month. It’s also possible for active employees at larger companies (who can delay Part B while they are still working) to be paying more than $300/month in premiums for their employer-sponsored coverage, depending on how generously the employer subsidizes the coverage.

- Beneficiaries with higher incomes who have to pay higher premiums for Medicare Part B and Part D. If you’re subject to this income-related monthly adjustment amount (IRMAA), which currently starts at $88,000 for a single individual and $176,000 for a married couple, you can appeal the surcharge if your financial circumstances have changed and you believe you should no longer be assessed the additional premiums.

If you didn’t get a chance to weigh in on our survey, or if you have a unique premium situation, we’d love to hear from you in the comment section below.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org. Her state health exchange updates are regularly cited by media who cover health reform and by other health insurance experts.